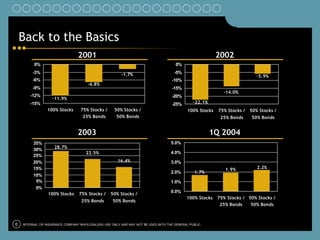

1. Back to the Basics

2001 2002

0% 0%

-3% -1.7% -5%

-5.9%

-6% -10%

-6.8%

-9% -15%

-14.0%

-12% -20%

-11.9%

-15% -25% -22.1%

100% Stocks 75% Stocks / 50% Stocks / 100% Stocks 75% Stocks / 50% Stocks /

25% Bonds 50% Bonds 25% Bonds 50% Bonds

2003 1Q 2004

35% 5.0%

28.7%

30%

22.5% 4.0%

25%

20% 16.4% 3.0%

15% 1.9% 2.2%

2.0% 1.7%

10%

5% 1.0%

0%

0.0%

100% Stocks 75% Stocks / 50% Stocks /

100% Stocks 75% Stocks / 50% Stocks /

25% Bonds 50% Bonds

25% Bonds 50% Bonds

0 INTERNAL OR INSURANCE COMPANY WHOLESALERS USE ONLY AND MAY NOT BE USED WITH THE GENERAL PUBLIC.

2. Who Cares?

Asset Allocation Matters Most

Stock Selection

l According to a key study of 4.6%

Other

pension fund performance*, Market Timing 2.2%

the overwhelming determinant 1.7%

of the success or failure of an

investment strategy is how the

assets were divided among the

various asset classes (stocks,

bonds, cash equivalents), and not

what securities were owned or

when they were bought or sold.

Asset Allocation Decision

91.5%

1 INTERNAL OR INSURANCE COMPANY WHOLESALERS USE ONLY AND MAY NOT BE USED WITH THE GENERAL PUBLIC.

3. StorySelling

Imagine a baseball soaring towards a

pane glass window. The risk that the

baseball would ruin the entire window is

pretty high.

If a baseball hits a traditional divided

window, the damage could be limited to

a single pane. The same concept applies

to investing.

A portfolio with just a single type of

investment can leave you at greater risk.

Diversification can help limit that risk.

2 INTERNAL OR INSURANCE COMPANY WHOLESALERS USE ONLY AND MAY NOT BE USED WITH THE GENERAL PUBLIC.

4. Diversify—Winners Rotate

Best Performing Asset Class from 1990-2003

Value Blend Growth

1990 Large-Cap

1998 >$7.75 Bn

1995 Mid-Cap

1993

1999 $1.3 Bn to $7.75 Bn

1992 1996 1991

1997 2000 1994 Small-Cap

<$1.3 Bn

2001 2002 2003

3 INTERNAL OR INSURANCE COMPANY WHOLESALERS USE ONLY AND MAY NOT BE USED WITH THE GENERAL PUBLIC.

5. Don’t be a “Johnny Come Lately”

Percentage Performance One-Year Later

250

216.42

200

150 124.99

97.98 87.84

100

56.16 58.09

50 38.64 37.24

22.06

3.82

0

-7.10 -9.44

-31.26 -21.77

-50

1996 1997 1997 1998 1998 1999 1999 2000 2000 2001 2001 2002 2002 2003

Year’s Top 25 Funds Same Funds One Year Later

4 INTERNAL OR INSURANCE COMPANY WHOLESALERS USE ONLY AND MAY NOT BE USED WITH THE GENERAL PUBLIC.

6. Case Study: Chasing Returns

Can Lead to Disappointment

History has shown that generally buy-and-hold investors who maintained a

well-allocated portfolio tended to fare better than those who

chased market trends.

Chasing highest returns:

$100,000 invested in previous $107,006

year’s high performer

Chasing lowest returns:

$100,000 invested in previous $116,345

year’s low performer

Buy and Hold:

A one-time $100,000

investment distributed evenly $127,002

over six market indices

1993 – 2002

5 INTERNAL OR INSURANCE COMPANY WHOLESALERS USE ONLY AND MAY NOT BE USED WITH THE GENERAL PUBLIC.

7. Value and Growth: Own Them Both

Style Rotation—Beyond Our Control

50%

40%

30%

20%

10%

0%

-10%

-20%

-30%

90

91

92

93

94

95

96

97

84

85

86

87

88

89

02

03

98

99

00

01

19

19

19

19

19

19

19

19

19

19

19

19

19

19

20

20

19

19

20

20

Russell 1000® Value Russell 1000® Growth

6 INTERNAL OR INSURANCE COMPANY WHOLESALERS USE ONLY AND MAY NOT BE USED WITH THE GENERAL PUBLIC.

8. The Van Kampen 50/50 Solution

A Balanced Solution—Within Our Control

50% VK Emerging Growth LIT

50% VK Growth and Income LIT

7 INTERNAL OR INSURANCE COMPANY WHOLESALERS USE ONLY AND MAY NOT BE USED WITH THE GENERAL PUBLIC.

9. A Van Kampen Solution vs. S&P500®

A Core Holding With Impressive Relative Performance

100% S&P 500® Van Kampen 50/50

5 year average annual return 5 year average annual return

through 12/31/03: through 12/31/03:

4.16% 11.45%

8 INTERNAL OR INSURANCE COMPANY WHOLESALERS USE ONLY AND MAY NOT BE USED WITH THE GENERAL PUBLIC.

10. VK 50/50 * vs. S&P 500®

$250,000

$200,000

$156,650

$150,000

$100,000

$124,944

$50,000

$0

1997 1998 1999 2000 2001 2002 2003

VK 50/50 S&P 500

A $31,706 Advantage

9 INTERNAL OR INSURANCE COMPANY WHOLESALERS USE ONLY AND MAY NOT BE USED WITH THE GENERAL PUBLIC.

11. Performance Review

Average Annual Total Return Percentages (Periods Ending June 30, 2004)

Year-To- Since

Date 1 Year 3 Year 5 year Inception

LIT Emerging Growth Portfolio 2.39 14.97 -8.37 -1.91 10.75

(Inception: 7/03/1995)

LIT Growth and Income Portfolio 3.48 20.02 3.09 5.48 10.55

(Inception: 12/23/1996)

10 INTERNAL OR INSURANCE COMPANY WHOLESALERS USE ONLY AND MAY NOT BE USED WITH THE GENERAL PUBLIC.

12. The Solution—

Experience on your Team

The Growth and Income Team

l 5 team members with a combined 45 years of experience

l The management team looks for undervalued companies

that are experiencing positive change that they believe

may provide superior returns relative to the market.

l The team seeks positive returns through growth and

income.

The Emerging Growth Team*

l 6 team members with a combined 90 years of experience

l The fund’s style of investing has been around for over

three decades and many market cycles.

l The team has consistently stuck to this style of looking for

stocks with growing earnings.

Team members will change without notice.

11 INTERNAL OR INSURANCE COMPANY WHOLESALERS USE ONLY AND MAY NOT BE USED WITH THE GENERAL PUBLIC.

13. Experience Matters

Experience is More than Just An Asset in Down Markets

Growth of $10,000: March 1994 – March 2004

Over the past 10 years, which $30,000 $28,394

encompassed both the bull

$27,500

markets, funds with experienced

managers have returned an $25,000

$23,673

average of 10.96% annually.

$22,500

Managers with less experience

delivered 9.36% over the same $20,000

period. Avg. return of funds Avg. return of funds

run by manager w/ run by manager w/

10 years or less 10 years or more

experience experience

12 INTERNAL OR INSURANCE COMPANY WHOLESALERS USE ONLY AND MAY NOT BE USED WITH THE GENERAL PUBLIC.