Pacc offshore services_holdings_ltd._(17_april_2014) (1)

•

2 gefällt mir•1,526 views

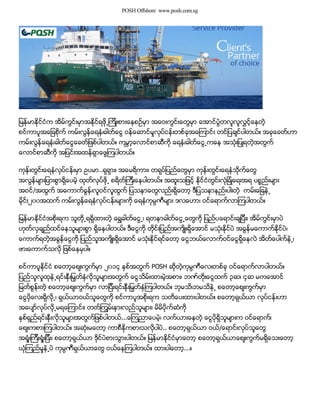

POSH PACC OFFSHORE SERVICES HOLDING Singapore

Empfohlen

Weitere ähnliche Inhalte

Mehr von Zaw Aung

Mehr von Zaw Aung (20)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

Pacc offshore services_holdings_ltd._(17_april_2014) (1)

- 1. POSH Offshore www.posh.com.sg ျမန္မာႏိုင္ငံက အိမ္ကြင္းမွာအႏိုင္ရဖို႕ၾကိဳးစားေနစဥ္မွာ အေဝးကြင္းေတြမွာ ေအာင္ပြဲတလူလူလႊင့္ေနတဲ့ စင္ကာပူအေျခစိုက္ ကမ္းလြန္ေရနံ၊ဓါတ္ေငြ ဝန္ေဆာင္မႈလုပ္ငန္းတစ္ခုအေၾကာင္း တင္ျပခ်င္ပါတယ္။ အခုေခတ္ဟာ ကမ္းလြန္ေရနံ၊ဓါတ္ေငြေခတ္ျဖစ္ပါတယ္။ ကမၻာ့ေလာင္စာဆီကို ေရနံ၊ဓါတ္ေငြ႕ကေန အသံုးျပဳရတဲ့အတြက္ ေလာင္စာဆီကို အျပင္းအထန္ရွာေဖြၾကပါတယ္။ ကုန္းတြင္းေရနံလုပ္ငန္းမွာ ဥပမာ..ရုရွား၊ အေမရိကား၊ တရုပ္ျပည္ေတြမွာ ကုန္းတြင္းေရနံသိုက္ေတြ အလြန္မ်ားျပားစြာရွိေပမဲ့ ထုတ္လုပ္ဖို႕ စရိတ္ၾကီးေနပါတယ္။ အထူးသျဖင့္ ႏိုင္ငံတြင္းလံုျခံဳေရးအရ ပစၥည္းမ်ား အဝင္/အထြက္ အေကာက္ခြန္၊လူဝင္လူထြက္ ျပသနာေတြလည္းရွိေတာ့ ဒီျပသနာနည္းပါးတဲ့ ကမ္းေျခနဲ႕ မိုင္း၂၀၀အထက္ ကမ္းလြန္ေရနံလုပ္ငန္းမ်ားကို ေရနံကုမၸဏီမ်ား ဒလေဟာ၊ ဝင္ေရာက္လာၾကပါတယ္။ ျမန္မာႏိုင္ငံအစိုးရက သူတို႕ရရွိထားတဲ့ ေရႊဓါတ္ေငြ႕၊ ရတနာဓါတ္ေငြ႕ေတြကို ျပည္ပေရာင္းခ်ျပီး၊ အိမ္ကြင္းမွာပဲ ဟုတ္လွခ်ည္ထင္ေနသူမ်ားစြာ ရွိေနပါတယ္။ ဒီေငြကို တိုင္းျပည္အက်ိဳးရွိေအာင္ မသံုးႏိုင္ပဲ အခြန္မေကာက္ႏိုင္ပဲ၊ ေကာက္ရတဲ့အခြန္ေငြကို ျပည္သူအက်ိဳးရွိေအာင္ မသံုးႏိုင္ရင္ေတာ့ ေငြဘယ္ေလာက္ဝင္ေငြရွိေနလဲ အိတ္ေပါက္နဲ႕၊ ဖားေကာက္သလို ျဖစ္ေနမွပါ။ စင္ကာပူႏိုင္ငံ စေတာ့ေစ်းကြက္မွာ ၂၀၁၄ ႏွစ္အတြက္ POSH ဆိုတဲ့ကုမၸဏီေလးတစ္ခု ဝင္ေရာက္လာပါတယ္။ ျပည္သူလူထုနဲ႕ရင္းႏွီးျမွတ္ႏွံလိုသူမ်ားအတြက္ ေငြသိမ္းထားမဲ့အစား၊ ဘဏ္တိုးေငြထက္ ၃ဆ၊ ၄ဆ မကေအာင္ ျမတ္စြန္းတဲ့ စေတာ့ေစ်းကြက္မွာ လာျပီးရင္းႏွီးျမွတ္ႏွံၾကပါတယ္။ ဘုမသိ၊ဘမသိနဲ႕ စေတာ့ေစ်းကြက္မွာ ေငြပိုေလးရွိလို႕၊ ရွယ္ယာဝယ္သူေတြကို စင္ကာပူအစိုးရက သတိေပးထားပါတယ္။ စေတာ့ရွယ္ယာ လုပ္ငန္းဟာ အေပ်ာ္လုပ္လို႕မရေၾကာင္း၊ တတ္ၾကြမ္းနားလည္သူမ်ား၊ မိမိပိုက္ဆံကို ႏွစ္ရွည္ရင္းႏွီးလိုသူမ်ားအတြက္ျဖစ္ပါတယ္...ေၾကညာေပမဲ့၊ လက္ယားေနတဲ့ ေငြပိုရွိသူမ်ားက ဝင္ေရာက္၊ ေစ်းကစားၾကပါတယ္။ အဆံုးမေတာ့ ကာစီႏိုကစားသလိုပါပဲ.. စေတာ့ရွယ္ယာ ဝယ္/ေရာင္းလုပ္သူေတြ အရံႈးၾကီးရံႈးျပီး၊ စေတာ့ရွယ္ယာ ဒိုင္ပဲစားသြားပါတယ္။ ျမန္မာႏိုင္ငံမွာေတာ့ စေတာ့ရွယ္ယာေစ်းကြက္မရွိေသးေတာ့ ယံုၾကည္မႈနဲ႕ပဲ ကုမၸဏီရွယ္ယာေတြ ဝယ္ေနၾကပါတယ္။ ထားပါေတာ့...။

- 2. POSH Offshore www.posh.com.sg စင္ကာပူ၏အိမ္ကြင္းပိုင္ဆိုင္မႈမ်ား စင္ကာပူမွာ ေရနံတစ္စက္မွ မထြက္ပါဘူး။ ဒါေပမဲ့ လူသားအရင္းျမစ္ Human Resource ကို ေကာင္းစြာအသံုးခ်ႏိုင္ပါတယ္။ လူေတြကို အရည္အခ်င္းျမွင့္တင္ေပးျပီး၊ ပညာသင္ေပးပါတယ္။ ေနာက္ျပီး စီမံခန္႕ခြဲမႈပညာကို အထူးအားကိုးပါတယ္။ စီမံခန္႕ခြဲရာမွာ အေျပာင္ေျမာက္ဆံုးကေတာ့ လာဘ္စားမႈမရွိသေလာက္ နည္းပါးေအာင္ အစိုးရက အထူးလုပ္ေဆာင္ပါတယ္။ ျခစားမႈရွိတဲ့ေနရာကို ယင္ေကာင္ေတြပဲလာေရာက္ရင္းႏွီးျမွတ္ႏွံမွာျဖစ္ပါတယ္။ လွပတဲ့ လိပ္ျပာ၊ ပုဇင္း၊ ငွက္မ်ား လာေရာက္ဖို႕ရာ Corruption Free ျဖစ္ေအာင္ဦးစြာလုပ္ေဆာင္ရပါတယ္။ ႏိုင္ငံအုပ္ခ်ဳပ္သူ ဝန္ၾကီးခ်ဳပ္နဲ႕ဝန္ၾကီးမ်ားကို လာဘ္စားမႈလံုးဝမရွိေအာင္ စီမံခန္႕ခြဲပါတယ္။ ဥပေဒစိုးမိုးေစပါတယ္။ စင္ကာပူရဲ့ လူ႕အခြင့္အေရး၊ လြတ္လပ္ခြင့္ခ်ဳပ္ကိုင္ထားေပမဲ့ စီးပြားေရးလြတ္လပ္ခြင့္ကို တရားမွ်တစြာ ယွဥ္ျပိဳင္ေစပါတယ္။ ဒါေၾကာင့္ စင္ကာပူႏိုင္ငံဟာ ကမၻာ့အၾကီးဆံုး ေရနံေလွာင္ကန္မ်ား၊ ကမၻာ့အၾကီးဆံုး ေရနံခ်က္စက္ရံုမ်ား၊ ကမၻာ့အၾကီးဆံုး သေဘၤာက်င္း၊ သေဘၤာနဲ႕ကမ္းလြန္ေရနံတူးစင္၊ ေရနံတူးသေဘၤာမ်ားေဆာက္လုပ္၊ ျပဳျပင္ျခင္းကို ေအာင္ျမင္စြာလုပ္ေဆာင္ခဲ့ပါတယ္။ အိမ္ကြင္းမွာ သေဘၤာလုပ္ငန္းကို စနစ္တက်လုပ္ေဆာင္၊ ေအာင္ျမင္လာေတာ့ ကမၻာ့သေဘၤာၾကီး ေတာ္ေတာ္မ်ားမ်ားဟာ စင္ကာပူမွာ မွတ္ပံုတင္ၾကပါတယ္။ စင္ကာပူမွာနားျပီး၊ ကုန္စည္ျဖည့္ဆည္း၊ သေဘၤာသား အတက္/အဆင္းေတြ လုပ္ၾကပါတယ္။ သေဘၤာကုမၸဏီရံုးမ်ား၊ ေရနံကုမၸဏီရံုးမ်ား။ ဘဏ္မ်ားစြာ လာေရာက္အေျခခ်ၾကပါတယ္။ ဒါက အိမ္ကြင္းမွာ သေဘၤာလုပ္ငန္း၊ ကမ္းလြန္ေရနံလုပ္ငန္း ဘယ္လိုအႏိုင္ရေအာင္ ကစားခဲ့ေၾကာင္း ႏွစ္၄၀ သမိုင္းျဖစ္ပါတယ္။ အေဝးကြင္းမွာပိုင္ဆိုင္မႈမ်ားျဖန္႕ထားျခင္း အိမ္ကြင္းမွာ အပိုင္အႏိုင္ကစားျပီးခ်ိန္မွာေတာ့ အေဝးကြင္းကို သြားကန္ဖို႕လုပ္ရပါတယ္။ စင္ကာပူပိုင္ဆိုင္လာတဲ့ မိေဆြမ်ား၊ Customer၊ နည္းပညာရွင္မ်ား၊ ေငြေၾကးမ်ားကို ျပည္တြင္းမွာပဲ ထားလို႕ေနရာမရွိေတာ့ပါဘူး။ အျမတ္ပိုမ်ားမ်ားရတဲ့ ျပည္ပကိုပို႕ရပါေတာ့တယ္။ နည္းမ်ိဳးစံုနဲ႕ အေဝးကြင္း ဥေရာပ၊ အေမရိက၊ ၾသစေၾတးလွ်၊ တရုပ္ျပည္ ..စတဲ့ႏိုင္ငံမ်ားဆီ ရင္းႏွီးျမွတ္ႏွံပါတယ္။ စက္မႈဇံုမ်ားတည္ေဆာက္ေပးျခင္း၊ ဘဏ္လုပ္ငန္းမ်ား စတဲ့လုပ္ငန္းမ်ားမွာ၊ ကမ္းလြန္ေရနံလုပ္ငန္းရဲ့ ဝန္ေဆာင္မႈလုပ္ငန္းကို ဝင္ေရာက္ခဲ့ပါတယ္။ POSH ကုမၸဏီရဲ့ ဝန္ေဆာင္မႈလုပ္ငန္းကေတာ့ ကမ္းလြန္ေရနံတူး၊ သယ္ယူေနတဲ့ ေရနံတူးစဥ္၊ သေဘၤာၾကီးမ်ားကို ပစၥည္းပို႕ေပးျခင္း၊ ဆြဲယူျခင္း၊ တြန္းေပးျခင္း၊ မီးေလာင္ပါက ျငိမ္းသတ္ေပးျခင္း၊ စတဲ့ ဝန္ေဆာင္မႈမ်ားကို လုပ္ပါတယ္။ ရွဲ၊ ဘီပီ Shell, BP စတဲ့ အလြန္ခ်မ္းသာလွတဲ့ ေရနံကုမၸဏီၾကီးမ်ားကို ဆြဲသေဘၤာမ်ား ငွားျခင္းလုပ္ငန္းျဖစ္ပါတယ္။ စေတာ့ေစ်းကြက္ကို ဝင္လာျပီဆိုေတာ့ က်ိတ္ျပီး၊ တိတ္တိတ္ေလး စီးပြားလုပ္လုိ႕မရေတာ့ပါဘူး။ ပြင့္လင္းျမင္သာစြာနဲ႕ လုပ္ရပါေတာ့တယ္။ POSH ကုမၸဏီရဲ့ ဝန္ထမ္းမ်ားဟာ လုပ္ငန္းေအာင္ျမင္မႈအတြက္ အလြန္အေရးၾကီးပါတယ္။ စင္ကာပူမွာ စနစ္တက်လုပ္ကိုင္တဲ့ ကမၻာ့အဆင့္ သေဘၤာလိုင္ၾကီး နက္ပကြ်န္း NOL သေဘၤာလိုင္ၾကီးရွိပါတယ္။ အဲဒီသေဘၤာလိုင္းမွာ လုပ္ကိုင္ေနသူမ်ားကို အဓိက ဝန္ထမ္းမ်ားအျဖစ္ ေခၚယူခန္႕ထားပါတယ္။ ဒါေၾကာင့္

- 3. POSH Offshore www.posh.com.sg စီမံခန္႕ခြဲမႈနည္းစနစ္ဟာ NOL System ကို အေျခခံထားတဲ့အတြက္၊ POSH ကုမၸဏီဟာ သက္တမ္းႏုေပမဲ့၊ ဝန္ထမ္းမ်ားကေတာ့ အလြန္အေတြ႕ၾကံဳရင့္က်က္သူမ်ားျဖစ္ပါတယ္။ ကုမၸဏီရဲ့ ပိုင္ဆိုင္မႈေတြဟာ စင္ကာပူမွာမရွိပါဘူး။ သေဘၤာမ်ားျဖစ္တဲ့အတြက္ ကမၻာအႏွံ႕ကို ျဖန္ခ်ထားပါတယ္။ ကမၻာေပၚမွာ ဆြဲသေဘၤာအမ်ားဆံုး ပိုင္ေၾကာင္း၊ ဒီလို ကမ္းလြန္ေရနံဝန္ေဆာင္မႈကို ကမၻာ့ထိပ္တန္း၅ခုထဲမွာ ပါေၾကာင္း စေတာ့ရွယ္ယာေစ်းကြက္မွာ ၾကြားဝါထားပါတယ္။ အဲဒီ ၁.၈ ဘီလွ်ံနဲ႕ေပါင္းရင္ စင္ကာပူစေတာ့ေစ်းကြက္မွာ ကမ္းလြန္ေရနံကုမၸဏီမ်ားရဲ့ ပိုင္ဆိုင္မႈ စုစုေပါင္းဟာ ၅၀ ဘီလွ်ံရွိသြားျပီလို႕ စင္ကာပူအစိုးရက ေၾကျငာပါတယ္။ POSH က ၾကြားဝါမယ္ဆိုလဲ ရပါတယ္။ ပြင့္လင္းျမင္သာစြာလုပ္ကိုင္တဲ့ စီးပြားေရးလုပ္ငန္းျဖစ္ပါတယ္။ ၂၀၀၈မွာ ေဒၚလာသန္း၄၀၀ တန္ဖိုးကေန အခု ၂၀၁၄ (၆ႏွစ္အတြင္း) ေဒၚလာသန္း ၁၈၀၀ 1.8 billion dollar တဟုန္ထိုး တိုးတက္စီးပြားျဖစ္လာပါတယ္။ အထူးသျဖင့္ အာဖရိက၊ အေရွ႕အလယ္ပိုင္း၊ အေရွ႕ေတာင္အာရွေတြမွာ ကန္ထရိုက္ေတြရပါတယ္။ အေမရိက၊ ၾသစေၾတးလ်ား၊ ဥေရာပေတြမွာလည္း သေဘၤာမ်ား ငွားထားရပါတယ္။ စေတာ့ေစ်းကြက္ကို ဝင္လာတာနဲ႕အေရာင္းအဝယ္ေကာင္းပါတယ္။ ကုမၸဏီရဲ့ လက္ရွိပိုင္ဆိုင္မႈဟာ ကန္ေဒၚလာ ၁.၈ဘီလ်ံ ရွိျပီး၊ ရွယ္ယာတစ္ခုကို ၁.၂ေဒၚလာနဲ႕ စင္ကာပူစေတာ့ေစ်းကြက္မွာ စတင္ပါတယ္။ ေလာေလာဆယ္ ေဒၚလာသန္း၄၀၀ ကန္ထရိုက္နဲ႕သေဘၤာေဆာက္တဲ့လုပ္ငန္းမ်ား ရရွိထားတယ္လို႕ ေၾကျငာပါတယ္။ ကမ္းလြန္ေရနံ ဝန္ေဆာင္မႈလုပ္ငန္းမ်ား မွန္ကန္တဲ့ရင္းႏွီးျမွတ္ႏွံသူမ်ားကို ဆြဲေဆာင္ဖို႕ ျမန္မာျပည္က စီးပြားလုပ္ငန္းမ်ားလို႕ ရႈိ၊ ကြယ္ဝွက္လုပ္လို႕မရပါဘူး။ ပြင့္လင္းျမင္သားစြာ လုပ္ရမွာျဖစ္ပါတယ္။ ကမၻာ့ထိပ္တန္း ေရနံကုမၸဏီမ်ားအတြက္ ဝန္ေဆာင္မႈလုပ္ေပးရေတာ့ ကိုယ့္ရဲ့စြမ္းေဆာင္ႏိုင္မႈကို အတိက်ေျပာရပါတယ္။ ေျပာတဲ့အတိုင္း မလုပ္ႏုိင္ရင္ စီးပြားပ်က္မွာျဖစ္ပါတယ္။ ကုမၸဏီပိုင္ဆိုင္တဲ့ သေဘၤာေပါင္း ၁၂၅ခု ရွိပါတယ္၊ ဘယ္ေလာက္တန္ဖိုးရွိတယ္ဆိုတာ စေတာ့ဝက္ဆိုဒ္မွာ ပြင့္လင္းစြာေၾကျငာထားပါတယ္။ Deep Sea AHTS, AHT, Mudboat (PSV), Submersible Barge,Towing Tug,

- 4. POSH Offshore www.posh.com.sg Deck/Tank Barge, Container Barge, Accommodation Vessel စတဲ့သေဘၤာမ်ားျဖစ္ပါတယ္။ ေရနံတူးစဥ္မ်ားမွာ အလုပ္လုပ္တဲ့ အင္ဂ်င္နီယာ၊ အလုပ္သမားေတြကို အလုပ္ခ်ိန္ျပီးရင္ ျပန္နားဖို႕ ေဟာ္တင္သေဘၤာမ်ား Accommodation Vessel လည္းေတာ္ေတာ္ အလုပ္ျဖစ္ပါတယ္။ အလြန္တန္ဖိုးၾကီးတဲ့အတြက္ အလုပ္သမားအဆင့္ဆိုလဲ အထူးၾကြမ္းက်င္ရပါတယ္။ အသက္ကယ္၊ ဟယ္လီေကာ္ပတာ သင္တန္း၊ မတတ္မေနရ တက္ရပါတယ္။ ေဆးလိပ္အရက္၊ မူးယစ္လံုးဝ ကင္းရွင္းပါတယ္။ လူက အေရးၾကီးဆံုးျဖစ္ေတာ့ ကမ္းလြန္အလုပ္သမားအားလံုး စိတ္ေရာ၊ကိုယ္ပါ သန္႕ရွင္းဖို႕ အထူးၾကပ္မတ္ပါတယ္။ လစာလည္း ေကာင္းေကာင္းေပးထားပါတယ္။ သေဘၤာသားတစ္ေယာက္ကို တစ္လ ေဒၚလာ၅၀၀၀အထက္ ေပးျပီး၊ ပညာရွင္မ်ားကို ေဒၚလာေသာင္းခ်ီေပးပါတယ္။ သေဘၤာဆြဲတဲ့လုပ္ငန္းမွာ၊ ေလွာင္ကန္ပံုစံလုပ္တဲ့သေဘၤာမ်ား၊ ေရနံသန္႕စင္တဲ့ FPSO သေဘၤာၾကီးမ်ား ကို ကမ္းလြန္ေရနံတြင္းေနရာထိေအာင္ ဆြဲသြားေပးရပါတယ္။ ဆြဲသေဘၤာေတြဟာ အင္ဂ်င္ပါဝါ အရမ္းျမင့္ပါတယ္။ ျမင္းေကာင္ေရ ၁၈၀၀၀ တစ္ေသာာင္းရွစ္ေထာင္ေက်ာ္၊ ရွိပါတယ္။ ဆြဲအားျမင့္ သေဘၤာတစ္စင္းကို ေဒၚလာသန္း၂၀ ကေန၊ ေဒၚလာသန္း၅၀ အထိ တန္ဖိုးသတ္မွတ္ထားပါတယ္။ ေရနံတူးစဥ္အနားမွာ ေရနံကုမၸဏီမ်ားလိုအပ္တဲ့ပစၥည္းမ်ားကို အျမန္သယ္ေဆာင္ျပီး၊ ပို႕ေပးရပါတယ္။ ေရနံတူးစဥ္ဟာ ကုန္ထုတ္လုပ္ငန္းလုပ္ေနတဲ့အတြက္ ပစၥည္းလာပို႕တဲ့ သေဘၤာငယ္မ်ားနဲ႕ တိုက္မိ၊ ထိမိ လံုးဝမျဖစ္ဖို႕လိုပါတယ္။ ေနာက္ပိုင္းမွာ ေရနံတူးစဥ္မ်ားရဲ့ တန္ဖိုးဟာ ေဒၚလာဘီလွ်ံေပါင္း မ်ားစြာရွိေတာ့ တိုက္မိ၊ထိမိ၊ မီေလာင္မႈေတြ လံုးဝအျဖစ္မခံႏိုင္ပါဘူး။ ပစၥည္းပို႕တဲ့ သေဘၤာငယ္မ်ားမွာ Dynamic Position ဆိုတဲ့ DP System ကိုတပ္ဆင္ထားရပါတယ္။ အလြန္စြမ္းအားျမင့္တဲ့ ဂ်င္နေရတာ၊ မိုတာမ်ားနဲ႕ သေဘၤာကို GPS သတ္မွတ္ထားတဲ့ေနရာမွာ၊ တစ္မီတာအတြင္းေလာက္၊ ျငိမ္ေနေအာင္ ေရွ႕ေနာက္၊ ဘယ္ညာ ပန္ကာၾကီးမ်ား Bow Truster နဲ႕လိုအပ္သလို ေမာင္းရပါတယ္။ ပင္လယ္ေရအလြန္နက္ေတာ့ ေက်ာက္စူးခ်ဖို႕လည္းမျဖစ္ႏိုင္လို႕ DP စနစ္ရွိတဲ့သဘၤာမ်ားကိုပဲ ငွားရမ္းၾကပါတယ္။ ေနာက္ပိုင္းမွာ DP စနစ္ေကာင္းမွာ သေဘၤာသတ္မွတ္တဲ့ ေနရာမွာ အတိက်ရွိမွာျဖစ္လို႕၊ ပိုျပီးေကာင္းမြန္တဲ့ DP1, DP2, DP3 စနစ္မ်ားလိုအပ္လာပါတယ္။ DP2 ဆိုတာကေတာ့ DP ထိန္းခ်ဳပ္မႈစနစ္ ၂ခုရွိတယ္ ဆိုတဲ့သေဘာပဲျဖစ္ပါတယ္။ တစ္ခုပ်က္ရင္ ေနာက္တစ္ခုသံုးႏိုင္မယ္။ ကမ္းလြန္ေရနံတူးစင္နဲ႕ ထိမိ၊ခိုက္မိ မျဖစ္ဖို႕ ပိုျပီးစိတ္ခ်ရပါတယ္။ နိဂံုး အေဝးကြင္းကို ကန္ႏိုင္ဖို႕ အိမ္ကြင္းမွာ ဦးစြာအႏိုင္ကန္ႏိုင္မွျဖစ္ပါမယ္။ ညစ္ပတ္ျပီးအႏိုင္ယူတဲ့ နည္းလမ္းနဲ႕ အႏိုင္ယူလို႕ရပါတယ္။ အစိုးရနဲ႕အာဏာပိုင္မ်ားက လာေရာက္လုပ္ကိုင္တဲ့ ႏိုင္ငံျခားကုမၸဏီအေပၚ ညစ္ပတ္အႏိုင္ယူရင္၊ ႏိုင္ငံျခားကုမၸဏီကလည္း ကမၻာ့တရားရံုးမွာ ျပန္ျပီးတရားစြဲမွာ ျဖစ္ပါတယ္။ တရာတေဘာင္ ျဖစ္လာရင္ေတာ့ ကုမၸဏီေကာင္းေတြ လာဖို႕ေျခလွမ္းရုတ္သိမ္းသြားမွာပါ။ စီးပြားေရးလုပ္ရာမွာ စနစ္တက်လုပ္ေဆာင္ဖို႕ဆိုတာ ပြင့္လင္းျမင္သာစြာ လုပ္ေဆာင္မွျဖစ္မွာပါ။ ညစ္ပတ္တဲ့ ႏိုင္ငံျခားကုမၸဏီမ်ားနဲ႕ ညစ္ပတ္တဲ့ျမန္မာျပည္တြင္းက အာဏာပိုင္မ်ား လာဘ္ ေတာင္းရမ္းေနရင္၊ ကုမၸဏီေတြက အခြန္မေပးဘူးျငင္းႏိုင္ပါတယ္။ ကုမၸဏီက အခြန္မေပးႏိုင္ရင္ တိုင္းျပည္လူထု အလြန္နစ္နာပါတယ္။

- 5. POSH Offshore www.posh.com.sg အေဝးကြင္းကို ကန္ေနတဲ့ စင္ကာပူ၊ မေလးရွား၊ ထိုင္း ႏိုင္ငံမ်ားနဲ႕ ပြင့္လင္းစြာ၊ အတူလုပ္ေဆာင္ဖို႕လိုပါတယ္။ ကိုယ္နဲ႕အဆင့္တူမ်ားေတာင္မဟုတ္ပါဘူး။ အေရွ႕ေတာင္အာရွႏိုင္ငံမ်ားဟာ ျမန္မာႏိုင္ငံထက္ အမ်ားၾကီးသာပါတယ္။ စီးပြားေရးလုပ္ရာမွာ ကိုယ္နဲ႕အဆင့္တူေတြနဲ႕ တြဲလုပ္တာ အေကာင္းဆံုးပါ။ ကိုယ့္ထက္ အရမ္းခ်မ္းသာတဲ့လူနဲ႕ စီးပြားေပါင္းလုပ္ရင္၊ ကိုယ္ပဲခံရမွာေသခ်ာပါတယ္။ ဒါေၾကာင့္ ျမန္မာႏိုင္ငံရဲ့ ျပဳျပင္ေျပာင္းလဲမႈေတြမွာ အေရွ႕ေတာင္အာရွႏိုင္ငံမ်ားဆီက စံနမူနာယူ၊ ပူးေပါင္းလုပ္ေဆာင္ႏိုင္မယ္.. လို႕ေမွ်ာ္လင့္ပါတယ္။ သေဘၤာဆြဲလုပ္ငန္း ကမ္းလြန္ေရနံတူးစဥ္အနီး၊ ဝန္ေဆာင္မႈလုပ္ငန္းမ်ား

- 6. PROSPECTUS DATED APRIL 17, 2014 (Registered by the Monetary Authority of Singapore on April 17, 2014) This document is important. If you are in any doubt as to the action you should take, you should consult your legal, financial, tax or other professional adviser. This is the initial public offering of the ordinary shares (our “Shares”) of PACC Offshore Services Holdings Ltd. (our “Company”). We are issuing 252,020,000 new Shares for subscription by investors at the Offering Price (as defined below). The Offering (as defined below) comprises: (i) an international offering to investors, including institutional and other investors in Singapore (the “International Offering”), including 25,200,000 Shares (the “Reserved Shares”) reserved for the directors, management, employees and business associates of our Company, our subsidiaries and our joint ventures, and Kuok (Singapore) Limited (“KSL”) and its subsidiaries (including Pacific Carriers Limited (“PCL”) and its subsidiaries) who have contributed to our success to be determined by us at our sole discretion, and (ii) an offering to the public in Singapore (the “Public Offering”). The International Offering and the Public Offering (together, the “Offering”) will consist of an aggregate of 252,020,000 Shares (the “Offering Shares”). The offering price (the “Offering Price”) for each Offering Share is S$1.15. At the same time as but separate from the Offering, each of Hwang Investment Management Berhad and Fortress Capital Asset Management (M) Sdn Bhd (collectively, the “Cornerstone Investors”) has entered into a cornerstone subscription agreement with our Company (collectively, the “Cornerstone Subscription Agreements”) to subscribe for an aggregate of 85,605,000 new Shares at the Offering Price (the “Cornerstone Shares”), conditional upon the Management and Underwriting Agreement and Placement Agreement (each as defined herein) having been entered into and not having been terminated pursuant to their terms on or prior to the Listing Date (as defined here). The Offering is underwritten by DBS Bank Ltd. (“DBS Bank”), Merrill Lynch (Singapore) Pte. Ltd. (“Merrill Lynch”) and Oversea-Chinese Banking Corporation Limited (“OCBC Bank”) (together, the “Joint Issue Managers, Bookrunners and Underwriters”) at the Offering Price. In connection with the Offering, PCL (the “Over-allotment Option Provider”) has granted Merrill Lynch, as stabilising manager (the “Stabilising Manager”), acting on behalf of the Joint Issue Managers, Bookrunners and Underwriters, an over-allotment option (the “Over-allotment Option”), exercisable in whole or in part on one or more occasions from the date of commencement of dealing in our Shares on the Singapore Exchange Securities Trading Limited (the “SGX-ST”) (the “Listing Date”) until the earlier of (i) the date falling 30 days from the Listing Date, or (ii) the date when the Stabilising Manager or its appointed agent has bought, on the SGX-ST, an aggregate of 46,125,000 Shares, representing approximately 18.3% of the total Offering Shares, to undertake stabilising actions, to purchase from PCL up to an aggregate of 46,125,000 Shares (the “Additional Shares”) (representing approximately 18.3% of the total Offering Shares) at the Offering Price, solely to cover the over-allotment of the Offering Shares, if any. The exercise of the Over-allotment Option will not increase the total number of issued Shares immediately after completion of the Offering. Prior to the Offering, there was no public market for our Shares. An application has been made to the SGX-ST for permission to list all our issued Shares, the Offering Shares, the Cornerstone Shares, the Additional Shares, the Shares which may be issued upon the exercise of options to be granted under the POSH Share Option Plan (the “Option Shares”) and the Shares which may be issued upon the release of awards to be granted under the POSH Performance Share Plan (the “Performance Shares”) on the Mainboard of the SGX-ST. Such permission will be granted when our Shares have been admitted to the Official List of the SGX-ST. Acceptance of applications for the Offering Shares will be conditional PACC OFFSHORE SERVICES HOLDINGS LTD. Company Registration No.: 200603185Z Incorporated in Singapore on 7 March 2006 upon, among others, permission being granted by the SGX-ST to deal in and for quotation of all our issued Shares, the Offering Shares, the Cornerstone Shares, the Additional Shares, the Option Shares and the Performance Shares. Monies paid in respect of any application accepted will be returned to you, at your own risk, without interest or any share of revenue or other benefit arising therefrom if the Offering is not completed because the said permission is not granted or for any other reason, and you will not have any right or claim against us, the Over-allotment Option Provider or the Joint Issue Managers, Bookrunners and Underwriters. Our Company has received a letter of eligibility from the SGX-ST for the listing and quotation of all our issued Shares, the Offering Shares, the Cornerstone Shares, the Additional Shares, the Option Shares and the Performance Shares on the Mainboard of the SGX-ST. Our Company’s eligibility to list and admission of our Shares to the Official List of the SGX-ST is not to be taken as an indication of the merits of the Offering, our Company, any of our subsidiaries, our Shares (including the Offering Shares, the Cornerstone Shares, the Additional Shares, the Option Shares and the Performance Shares), the POSH Share Option Plan or the POSH Performance Share Plan. The SGX-ST assumes no responsibility for the correctness of any statements or opinions made or reports contained in this Prospectus. A copy of this Prospectus has been lodged with and registered by the Monetary Authority of Singapore (the “Authority” or “MAS”) on April 7, 2014, and April 17, 2014, respectively. The Authority assumes no responsibility for the contents of this Prospectus. Registration of this Prospectus by the Authority does not imply that the Securities and Futures Act, Chapter 289 of Singapore (the “Securities and Futures Act” or the “SFA”), or any other legal or regulatory requirements, have been complied with. The Authority has not, in any way, considered the merits of our Shares being offered for investment (or of the Additional Shares, where the Over-allotment Option is exercised). No Shares will be allotted on the basis of this Prospectus later than six months after the date of registration of this Prospectus with the Authority. Investing in our Shares involves risks. See “Risk Factors” for a discussion of certain factors to be considered in connection with an investment in our Shares. Nothing in this Prospectus constitutes an offer for securities for sale in the United States of America (“United States” or “U.S.”) or any other jurisdiction where it is unlawful to do so. The Offering Shares have not been, and will not be, registered under the United States Securities Act of 1933, as amended (the “Securities Act”) or the securities laws of any state of the United States and accordingly, may not be offered or sold within the United States (as defined in Regulation S under the Securities Act (“Regulation S”)). The Offering Shares are only being offered and sold outside the United States in offshore transactions as defined in, and in reliance on, Regulation S. For further details about restrictions on offers, sales and transfers of our Shares, see “Plan of Distribution”. Investors applying for Offering Shares by way of application forms or electronic applications (both as referred to in “Appendix G – Terms, Conditions and Procedures for Application for and Acceptance of the Offering Shares in Singapore”) in the Public Offering will pay the Offering Price on application, subject to refund of the full amount or, as the case may be, the balance of the application monies (in each case without interest or any share of revenue or other benefit arising therefrom and without any right or claim against us, the Over-allotment Option Provider or the Joint Issue Managers, Bookrunners and Underwriters), where (i) an application is rejected or accepted in part only, or (ii) the Offering does not proceed for any reason. Investors applying for the International Offering are required to pay the Offering Price. Offering in respect of 252,020,000 Offering Shares (subject to the Over-allotment Option) Offering Price: S$1.15 per Offering Share Joint Issue Managers, Bookrunners and Underwriters

- 7. This overview section is qualified in its entirety by, and should be read in conjunction with, the full text of this Prospectus. Meanings of capitalised terms used may be found in the sections entitled “Defined Terms and Abbreviations” and “Glossary of Technical Terms” of this Prospectus POSH’S COMPETITIVE STRENGTHS 1. Largest Asia-based international operator of offshore support vessels and one of the top 5 globally1 • Large, diversified fleet of 112 offshore support vessels2 2. Global reach with a proven international operating track record • POSH believes that the geographical diversification of its operations reduces dependence on and risk exposure to any single geographical market and/or customer 3. Strong parentage: a member of the Kuok (Singapore) Limited (“KSL”) Group • Dedicated offshore support vessel business of the KSL Group • POSH believes its strategic relationships with affiliated shipyards of the KSL Group will allow POSH to respond rapidly to changing market dynamics 4. Established reputation and long-standing relationships with key oil and gas industry players • Leading global shipyards and offshore engineering companies such as Saipem, Hyundai Heavy Industries, Technip Singapore and SapuraClough Offshore work with POSH on a regular basis • Established reputation and long-standing relationships with global oil and gas majors and international oil and gas contractors 5. Highly-experienced and committed management team • Chief Executive Officer and Executive Director, Mr. Seow Kang Hoe, Gerald, has more than 40 years’ experience in the shipping industry • Management team includes 12 shore-based Master Mariners and 23 Chief Engineers with an aggregate sea-going experience of more than 600 years3

- 8. LARGE, MODERN AND DIVERSE FLEET OF OFFSHORE SUPPORT VESSELS… • Vessels1 are designed with diesel electric propulsion and Clean-Design Notation and Green Passports, reducing and limiting the ship’s combustion machinery emissions and accidental sea pollution • Combined fleet of 112 vessels2, comprising: 14 Anchor Handling Tug Supply (“AHTS”) vessels, 13 Platform Supply Vessels (“PSVs”), 19 Anchor Handling Tugs (“AHTs”), 9 towing tugs, 20 barges, 5 accommodation vessels3, 23 harbour tugs, 4 crane barges and 5 support vessels • 15 Vessels4 on order and scheduled for delivery: Comprises 2 deck cargo barges, 2 ASD harbour tugs, 3 DP2 accommodation vessels, 3 DP2 AHTS, 2 DP3 SSAVs and 3 vessels which our joint ventures have on order • Services: anchor handling, ocean towage and installation, ocean transportation, heavy-lift, offshore accommodation, harbour towage and emergency response THE POSH FLEET2 Number 25 20 15 10 5 0 5 Support Vessels Crane Barges Harbour Tugs Offshore Supply Vessels Offshore Accomodation Harbour Services and Emergency Response Transportation and Installation 1 DP2 PSVs, DP2 accommodation vessels and DP3 SSAVs 2 As of December 31, 2013 3 Includes one vessel that is undergoing conversion into an accommodation vessel 4 As of the Latest Practicable Date. Not including one vessel undergoing conversion into an accommodation vessel Towing Tugs Barges PSV Accomodation AHTs AHTS Vessels 4 23 20 13 5 17 14 9 2

- 9. POSH IS THE LARGEST ASIA-BASED INTERNATIONAL OPERATOR OF OFFSHORE SUPPORT VESSELS AND ONE OF THE TOP FIVE GLOBALLY5 GLOBAL REACH WITH A PROVEN INTERNATIONAL OPERATING TRACK RECORD Mexico Nigeria Gabon India Malaysia 5 Based on Infield’s data on the number of vessels operated by POSH and the other major international providers of global support vessels New Caledonia Egypt China UAE Thailand Russia Venezuela Countries operated in over the years Countries currently operating in Singapore Angola Indonesia Australia Myanmar Vietnam Congo South Africa New Zealand Philippines Brazil UK Oman Italy Saudi Arabia Iran

- 10. 6. Well-positioned to capture market opportunities across all business segments • The youngest deepwater AHTS and PSV fleet and the youngest midwater AHTS and PSV fleet globally, with an average age of 2.3 and 2.2 years, as at December 31, 2013 respectively4 OFFSHORE SUPPLY VESSELS OFFSHORE ACCOMMODATION HARBOUR SERVICES AND EMERGENCY RESPONSE TRANSPORTATION AND INSTALLATION • 5 vessels3 (including one vessel undergoing conversion into a 198-person accommodation vessel) • Expected to operate the youngest high-berth accommodation vessels fleet in the world with the delivery of two 750-person DP3 SSAVs by end 20144 • Two 238-person DP2 accommodation vessels scheduled to be delivered by end 2014 • One 238-person DP2 accommodation vessel scheduled to be delivered by first quarter of 2015 • One of the largest deepwater AHT fleets in the world4 • Built up a track record in completing many demanding and high-value ocean towage projects, having successfully completed 53 floating system T&I contracts since 19913 • Awarded the transportation and installation contract for Ichthys Central Processing Facility (“CP Facility”), which is expected to be the world’s largest CP Facility installed to date when completed • Harbour Services business has been operating for over 10 years • One of the two main offshore support vessel operators globally to offer emergency response services which include salvage, wreck removal, rescue and oil-spill response services4 1 Based on data provided by Infield Systems Limited on the number of vessels operated by POSH and the other major international providers of global support vessels 2 As of December 31, 2013 3 As of the Latest Practicable Date 4 According to Infield Systems Limited

- 11. POSH’S STRATEGIES 1. MAINTAINING GROWTH MOMENTUM • Growing since incorporation in 2006 • Total assets have grown from US$35.7 million as at December 31, 2006 to US$1.8 billion as at December 31, 2013 • In-principle approval given by the Board for a capital expenditure budget of US$291.5 million for the further expansion of our fleet in the offshore supply vessels (“OSV”), transportation and installation and harbour services and emergency response business segments (including the acquisition of multifunctional support vessels (“MSV”)) (“Further Fleet Expansion”) - Plan to implement the Further Fleet Expansion in 2014 2. BROADEN FLEET DIVERSIFICATION • Expanding our fleet through the acquisition of larger and more sophisticated vessels • 15 vessels on order and scheduled for delivery and one vessel undergoing conversion into an accommodation vessel1 3. EXPAND INTO DEEPWATER OFFSHORE ACCOMMODATION AND OTHER HIGH-GROWTH ASSET CLASSES • Focus on high-capacity and high-specification offshore accommodation vessels • Exploring entry into the Inspection, Maintenance and Repair (“IMR”) segment and potential acquisition of IMR vessels 4. MAINTAIN HIGH SERVICE RELIABILITY 5. OPTIMISE CHARTER MIX FOR OSV AND OFFSHORE ACCOMMODATION FLEET • To provide stable revenue streams • Long-term charters: predictable and reliable cash flows • Short-term charters: benefit from higher day rates 6. EXPAND INTO NEW GEOGRAPHIC MARKETS WITH SIGNIFICANT GROWTH POTENTIAL • Australia, Indonesia, Latin America and the EMEA2 region Net Profit: 3-Year CAGR* of 67.4% 26.2 53.5 73.4 10.9 22 30.9 Net Profit (US$”million) Net Profit Margin (%)3 Year ended 31 December 2011 Year ended 31 December 2012 Year ended 31 December 2013 * Compounded annual growth rate 1 As of the Latest Practicable Date 2 Europe, Middle East and Africa 3 Derived by dividing net profit over revenue

- 12. TABLE OF CONTENTS Page Notice to Investors. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . iii Corporate Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . x Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 Risk Factors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29 Use of Proceeds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 60 Dividend Policy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 63 Capitalisation and Indebtedness . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64 Dilution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 66 Exchange Rates and Exchange Controls. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69 Selected Consolidated Financial Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 74 Selected Pro Forma Financial Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77 Management’s Discussion and Analysis of Financial Condition and Results of Operations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 81 Business . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 112 Government Regulations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 145 Management . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 156 Share-Based Incentive Plans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 171 Principal Shareholders . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 193 Interested Person Transactions and Potential Conflicts of Interest . . . . . . . . . . . . . . 198 Share Capital . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 219 Description of our Shares . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 223 Taxation. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 230 Plan of Distribution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 233 Clearance and Settlement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 242 Legal Matters . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 243 Independent Auditors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 244 Experts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 245 General and Statutory Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 246 Defined Terms and Abbreviations. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 253 i

- 13. Glossary of Technical Terms. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 257 Appendix A – Industry Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A-1 Appendix B – Letter from KPMG CF relating to the Mark-up for Shared Services . . B-1 Appendix C – Letter from KPMG CF relating to the Shareholders’ Mandate . . . . . C-1 Appendix D – Summary of Selected Articles of Association of our Company . . . D-1 Appendix E – List of Present and Past Principal Directorships of our Directors and Executive Officers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . E-1 Appendix F – List of Subsidiaries and Associated Companies . . . . . . . . . . . . . . . F-1 Appendix G – Terms, Conditions and Procedures for Application for and Acceptance of the Offering Shares in Singapore . . . . . . . . . . . . . . . G-1 Appendix H – Audited Consolidated Financial Statements for the Years Ended December 31, 2011, 2012 and 2013 . . . . . . . . . . . . . . . . . . . . . . . . . . H-i Appendix I – Unaudited Pro Forma Financial Statements for the Year Ended December 31, 2013. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . I-i Appendix J – List of Mandated Interested Persons . . . . . . . . . . . . . . . . . . . . . . . . . J-1 Appendix K – Independent Valuation Certificate . . . . . . . . . . . . . . . . . . . . . . . . . . . K-1 ii

- 14. NOTICE TO INVESTORS No person is authorised to give any information or to make any representation not contained in this Prospectus and any information or representation not so contained must not be relied upon as having been authorised by or on behalf of us, the Over-allotment Option Provider or the Joint Issue Managers, Bookrunners and Underwriters. Neither the delivery of this Prospectus nor any offer, sale or transfer made hereunder shall under any circumstances imply that the information herein is correct as of any date subsequent to the date hereof or constitute a representation that there has been no change or development reasonably likely to involve a material adverse change in our affairs, condition and prospects or our Shares since the date hereof. In the event any changes occur, where such changes are material or required to be disclosed by law, the SGX-ST and/or any other regulatory or supervisory body or agency, or if we otherwise determine, we and the Over-allotment Option Provider will make an announcement of the same to the SGX-ST and, if required, issue and lodge an amendment to this Prospectus or a supplementary document or replacement document pursuant to Section 240 or, as the case may be, Section 241 of the SFA and take immediate steps to comply with the said sections. Investors should take notice of such announcements and documents and upon release of such announcements or documents shall be deemed to have notice of such changes. None of us, the Over-allotment Option Provider, the Joint Issue Managers, Bookrunners and Underwriters or any of our or their affiliates, directors, officers, employees, agents, representatives or advisers are making any representation or undertaking to any investors in our Shares regarding the legality of an investment by such investor under appropriate investment or similar laws. In addition, investors in our Shares should not construe the contents of this Prospectus or its appendices as legal, business, financial or tax advice. Investors should be aware that they may be required to bear the financial risks of an investment in our Shares for an indefinite period of time. Investors should consult their own professional advisers as to the legal, tax, business, financial and related aspects of an investment in our Shares. The Offering Shares have not been, and will not be, registered under the Securities Act and accordingly, may not be offered or sold within the United States. The Offering Shares are only being offered and sold outside the United States in offshore transactions as defined in, and in reliance on, Regulation S. We and the Over-allotment Option Provider are subject to the provisions of the Securities and Futures Act and the Listing Manual regarding the contents of this Prospectus. In particular, if after this Prospectus is registered but before the close of the Offering, we and the Over-allotment Option Provider become aware of: (a) a false or misleading statement in this Prospectus; (b) an omission from this Prospectus of any information that should have been included in it under Section 243 of the Securities and Futures Act; or (c) a new circumstance that has arisen since this Prospectus was lodged with the Authority which would have been required by Section 243 of the Securities and Futures Act to be included in this Prospectus if it had arisen before this Prospectus was lodged, that is materially adverse from the point of view of an investor, we and the Over-allotment Option Provider may lodge a supplementary or replacement document with the Authority pursuant to Section 241 of the Securities and Futures Act. iii

- 15. Where applications have been made under this Prospectus to subscribe for and/or purchase the Offering Shares prior to the lodgment of the supplementary or replacement document and the Offering Shares have not been issued and/or transferred to the applicants, we and the Over-allotment Option Provider shall either: (i) within seven days from the date of lodgment of the supplementary or replacement document, provide the applicants with a copy of the supplementary or replacement document, as the case may be, and provide the applicants with an option to withdraw their applications; or (ii) treat the applications as withdrawn and cancelled and return all monies paid, without interest or any share of revenue or other benefit arising therefrom and at the applicant’s own risk, in respect of any applications received, within seven days from the date of lodgment of the supplementary or replacement document. Where applications have been made under this Prospectus to subscribe for and/or purchase the Offering Shares prior to the lodgment of the supplementary or replacement document and the Offering Shares have been issued and/or transferred to the applicants, we and the Over-allotment Option Provider shall either: (1) within seven days from the date of lodgment of the supplementary or replacement document, provide the applicants with a copy of the supplementary or replacement document, as the case may be, and provide the applicants with an option to return to us and the Over-allotment Option Provider, those Offering Shares that the applicants do not wish to retain title in; or (2) treat the issue and/or sale of the Offering Shares as void and return all monies paid, without interest or any share of revenue or other benefit arising therefrom and at the applicant’s own risk, in respect of any applications received, within seven days from the date of lodgment of the supplementary or replacement document. Any applicant who wishes to exercise his option to withdraw his application or return the Offering Shares issued and/or sold to him shall, within 14 days from the date of lodgment of the supplementary or replacement document, notify us and the Over-allotment Option Provider, whereupon we and the Over-allotment Option Provider shall, within seven days from the receipt of such notification, return the application monies without interest or any share of revenue or other benefit arising therefrom and at the applicant’s own risk. Under the Securities and Futures Act, the Authority may in certain circumstances issue a stop order (the “Stop Order”) to us and the Over-allotment Option Provider, directing that no or no further Offering Shares be allotted, issued or sold. Such circumstances will include a situation where this Prospectus (i) contains a statement which, in the opinion of the Authority, is false or misleading, (ii) omits any information that is required to be included in accordance with the Securities and Futures Act or (iii) does not, in the opinion of the Authority, comply with the requirements of the Securities and Futures Act. Where the Authority issues a Stop Order pursuant to Section 242 of the Securities and Futures Act: (A) in the case where the Offering Shares have not been issued and/or transferred to the applicants, the applications for the Offering Shares pursuant to the Offering shall be deemed to have been withdrawn and cancelled and we and the Over-allotment Option Provider, shall, within 14 days from the date of the Stop Order, pay to the applicants all monies the applicants have paid on account of their applications for the Offering Shares; or iv

- 16. (B) in the case where the Offering Shares have been issued and/or transferred to the applicants, the issue and/or sale of the Offering Shares shall be deemed void and we and the Over-allotment Option Provider shall, within seven days from the date of the Stop Order, pay to the applicants all monies paid by them for the Offering Shares. Where monies paid in respect of applications received or accepted are to be returned to the applicants, such monies will be returned at the applicants’ own risk, without interest or any share of revenue or other benefit arising therefrom, and the applicants will not have any claim against us, the Over-allotment Option Provider and the Joint Issue Managers, Bookrunners and Underwriters. The distribution of this Prospectus and the offer, subscription, purchase, sale or transfer of our Shares may be restricted by law in certain jurisdictions. We, the Over-allotment Option Provider and the Joint Issue Managers, Bookrunners and Underwriters require persons into whose possession this Prospectus comes to inform themselves about and to observe any such restrictions at their own expense and without liability to us, the Over-allotment Option Provider or the Joint Issue Managers, Bookrunners and Underwriters. This Prospectus does not constitute an offer of, or an invitation to purchase or subscribe for, any of our Shares in any jurisdiction in which such offer or invitation would be unlawful. Persons to whom a copy of this Prospectus has been issued shall not circulate to any other person, reproduce or otherwise distribute this Prospectus or any information herein for any purpose whatsoever nor permit or cause the same to occur. In connection with the Offering, the Over-allotment Option Provider has granted the Stabilising Manager, acting on behalf of the Joint Issue Managers, Bookrunners and Underwriters, the Over-allotment Option, exercisable in whole or in part on one or more occasions from the Listing Date until the earlier of (i) the date falling 30 days from the Listing Date, or (ii) the date when the Stabilising Manager or its appointed agent has bought, on the SGX-ST, an aggregate of 46,125,000 Shares, representing approximately 18.3% of the total Offering Shares, to undertake stabilising actions, to purchase from PCL up to an aggregate of 46,125,000 Additional Shares (representing 18.3% of the total Offering Shares) at the Offering Price, solely to cover the over-allotment of the Offering Shares, if any. The exercise of the Over-allotment Option will not increase the total number of issued Shares immediately after completion of the Offering. In connection with the Offering, the Stabilising Manager or its appointed agent may over-allot Shares or effect transactions which may stabilise or maintain the market price of our Shares at levels above those that would otherwise prevail in the open market. Such transactions may be effected on the SGX-ST and in other jurisdictions where it is permissible to do so, in each case in compliance with all applicable laws and regulations, including the Securities and Futures Act and any regulations thereunder. However, we cannot assure you that the Stabilising Manager or its appointed agent will undertake stabilising action. Such transactions may commence on or after the Listing Date and, if commenced, may be discontinued at any time and shall not be effected later than the earlier of (i) the date falling 30 days from the Listing Date, or (ii) the date when the Stabilising Manager or its appointed agent has bought, on the SGX-ST, an aggregate of 46,125,000 Shares, representing approximately 18.3% of the total Offering Shares, to undertake stabilising actions. v

- 17. NOTICE TO INVESTORS IN THE EUROPEAN ECONOMIC AREA This Prospectus is not a prospectus for the purposes of the Prospectus Directive as implemented in Member States of the European Economic Area. This Prospectus has been prepared on the basis that all offers of the Offering Shares will be made pursuant to an exemption under the Prospectus Directive from the requirement to produce a prospectus in connection with offers of the Offering Shares. Accordingly, any person making or intending to make any offer within the European Economic Area of the Offering Shares which are the subject of the offering contemplated in this Prospectus should only do so in circumstances in which no obligation arises for us or any of the Underwriters to produce a prospectus for such offers. The expression “Prospectus Directive” means Directive 2003/71/EC (and amendments thereto, including the 2010 PD Amending Directive, to the extent implemented in the relevant Member State), and includes any relevant implementing measure in the relevant Member State and the expression 2010 PD Amending Directive means Directive 2010/73/EU. FORWARD-LOOKING STATEMENTS This Prospectus contains forward-looking statements which are statements that are not historical facts, including statements about our beliefs and expectations. Forward-looking statements generally can be identified by the use of forward-looking terminology, such as “may”, “will”, “could”, “expect”, “anticipate”, “intend”, “plan”, “believe”, “seek”, “estimate”, “project” and similar terms and phrases. These statements include, among others, statements regarding our business strategy, future financial position and results, and plans and objectives of our management for future operations. Forward-looking statements are, by their nature subject to substantial risks and uncertainties, and investors should not unduly rely on such statements. Forward-looking statements reflect our current views with respect to future events and are not a guarantee of future performance. These statements are based on our management’s beliefs and assumptions, which in turn are based on currently available information. Although we believe the assumptions upon which these forward-looking statements are based are reasonable, any of these assumptions could prove to be inaccurate, and the forward-looking statements based on these assumptions could be incorrect. Actual results may differ materially from information contained in the forward-looking statements as a result of a number of factors, many of which are beyond our control, including: • our ability to obtain financing in the future to fund capital expenditures, acquisitions and other general corporate activities; • the availability of cash for payment of dividends; • our ability to obtain shareholder approval, if necessary, to implement any of our strategies or to undertake expansion plans; • the availability of vessels for purchase, the time which it may take to construct new vessels, or vessels’ useful lives; • general offshore market conditions and trends, including charter rates, vessel values, bunker fuel expenses and factors affecting vessel supply and demand; • the strength of world economies and currencies and general domestic and international political conditions; • changes in governmental rules and regulations or actions taken by regulatory authorities; and • other factors discussed under “Risk Factors”. vi

- 18. Because of these factors, we caution you not to place undue reliance on any of our forward-looking statements. Forward-looking statements we make represent our judgment on the dates such statements are made. New risks and uncertainties arise from time to time, and it is impossible for us to predict these events or how they may affect us. Save as required by all applicable laws of applicable jurisdictions, including the Securities and Futures Act, and/or rules of the SGX-ST, we assume no obligation to update any information contained in this document or to publicly release the results of any revisions to any forward-looking statements to reflect events or circumstances that occur, or that we become aware of, after the date of this Prospectus. INDUSTRY AND MARKET DATA This Prospectus includes market share and industry data and forecasts that we obtained from industry publications and surveys, reports of governmental agencies and internal company surveys. Infield Systems Limited (the “Independent Market Research Consultant”) was the primary source for third party industry data and forecasts. Industry publications and surveys and forecasts generally state that the information contained therein has been obtained from sources believed to be reliable, but there can be no assurance as to the accuracy or completeness of included information. While we, the Over-allotment Option Provider and the Joint Issue Managers, Bookrunners and Underwriters have taken reasonable actions to ensure that the information is extracted accurately and in its proper context, we, the Over-allotment Option Provider and the Joint Issue Managers, Bookrunners and Underwriters have not independently verified any of the data from third party sources or ascertained the underlying economic assumptions relied upon therein and neither we, the Over-allotment Option Provider nor the Joint Issue Managers, Bookrunners and Underwriters makes any representation as to the accuracy or completeness of that information. Statements as to our market position are based on the most currently available market data. The information and data contained in the report appearing in “Appendix A – Industry Overview” were taken from Infield’s databases and other sources available in the public domain. Infield has advised us that it accurately describes the offshore marine services market, subject to the availability and reliability of the data supporting the statistical and graphical information presented. Infield’s methodologies for collecting information and data, and therefore the information discussed in the report appearing in “Appendix A – Industry Overview”, may differ from those of other sources, and does not reflect all or even necessarily a comprehensive set of the actual transactions occurring in the offshore marine services market. Although we, the Over-allotment Option Provider and the Joint Issue Managers, Bookrunners and Underwriters believe the information and data in report appearing in “Appendix A – Industry Overview” to be accurate, we, the Over-allotment Option Provider and the Joint Issue Managers, Bookrunners and Underwriters have not independently verified the information or data. The source of all tables and charts in the report appearing in “Appendix A – Industry Overview” is Infield unless otherwise indicated. vii

- 19. CERTAIN DEFINED TERMS AND CONVENTIONS In this Prospectus, references to “S$” or “Singapore dollars” or “Singapore cents” are to the lawful currency of the Republic of Singapore, references to “US$”, “U.S. dollars” or “U.S. cents” are to the lawful currency of the United States of America, references to “Rp.” or “rupiah” are to the lawful currency of Indonesia, references to “peso” or “Mexican Peso” are to the lawful currency of Mexico, references to “£” are to the lawful currency of the United Kingdom, references to “C” are to Euro, the lawful currency of certain nations within the European Union, references to “R” are to the lawful currency of South Africa and references to “RM” are to the lawful currency of Malaysia. For the reader’s convenience, unless otherwise indicated, certain U.S. dollar amounts in this Prospectus have been translated into Singapore dollars based on the exchange rate of S$1.27 = US$1.00, quoted by Bloomberg L.P. on the Latest Practicable Date. However, such translations should not be construed as a representation that Singapore dollar or U.S. dollar amounts have been, could have been or could be converted into U.S. dollars or Singapore dollars, as the case may be, at the rate indicated, any particular rate or at all. See “Exchange Rates and Exchange Controls – Exchange Rates” for further information regarding rates of exchange between the Singapore dollar and the U.S. dollar. We have included the exchange rate quoted above in its proper form and context in this Prospectus. Bloomberg L.P. has not provided its consent, for the purposes of Section 249 of the Securities and Futures Act, to the inclusion of the exchange rate quoted above in this Prospectus, and is thereby not liable for such information under Sections 253 and 254 of the Securities and Futures Act. While we, the Over-allotment Option Provider and the Joint Issue Managers, Bookrunners and Underwriters have taken reasonable actions to ensure that the above exchange rate has been reproduced in its proper form and context, neither we, the Over-allotment Option Provider, the Joint Issue Managers, Bookrunners and Underwriters nor any other party has conducted an independent review of the information or verified the accuracy of the contents of the relevant information. All trademarks appearing herein are the property of their respective owners. In this Prospectus, references to the “Latest Practicable Date” refer to March 25, 2014. Any discrepancies in any tables, graphs or charts included in this Prospectus between the totals and the sums of the amounts listed are due to rounding. The information on our website or any website directly or indirectly linked to our website or the websites of any of our related corporations or other entities in which we may have an interest is not incorporated by reference into this Prospectus and should not be relied on. In this Prospectus, references to our “Company” or “POSH” are to PACC Offshore Services Holdings Ltd. and, unless the context otherwise requires, “we”, “us”, “our” and “our Group” refer to PACC Offshore Services Holdings Ltd. and its subsidiaries taken as a whole. Unless the context otherwise requires, references in this Prospectus to our vessels, fleet, vessel fleet or combined vessel fleet refer to vessels which POSH and its subsidiaries own, as well as vessels held through our joint ventures, which we account for as jointly controlled entities using the equity method, and references to and descriptions of our business in this Prospectus refer to the business carried out by our Group together with such joint ventures. All references to “our Board of Directors” or “our Directors” are to the board of Directors of PACC Offshore Services Holdings Ltd. In this Prospectus, the definitions and explanation of technical terms found in this section and “Defined Terms and Abbreviations” apply throughout where the context so admits. viii

- 20. Our customers named in this Prospectus are generally referred to, in this Prospectus, by their trade names. Our contracts with these customers are typically with an entity or entities in that customer’s group of companies. In addition, unless we indicate otherwise, all information in this Prospectus assumes (i) that the Over-allotment Option is not exercised; and (ii) that no Offering Shares have been re-allocated between the International Offering and the Public Offering. ix

- 21. CORPORATE INFORMATION Directors Kuok Khoon Ean (Chairman and Non-Executive Director) Seow Kang Hoe, Gerald (Chief Executive Officer and Executive Director) Wu Long Peng (Non-Executive Director) Teo Joo Kim (Non-Executive Director) Ahmad Sufian @ Qurnain Bin Abdul Rashid (Independent Director) Ma Kah Woh (Independent Director) Jude Philomen Benny (Lead Independent Director) Wee Joo Yeow (Independent Director) Company Secretary Tay Cheng Imm Dawn, Bachelor of Laws Registered Office 1 Kim Seng Promenade, #07-02 Great World City Singapore 237994 Principal Place of Business 1 Kim Seng Promenade, #06-01 Great World City Singapore 237994 Company Registration Number 200603185Z Over-allotment Option Provider Pacific Carriers Limited 1 Kim Seng Promenade, #07-02 Great World City Singapore 237994 Share Registrar Boardroom Corporate & Advisory Services Pte. Ltd. 50 Raffles Place #32-01 Singapore Land Tower Singapore 048623 Joint Issue Managers, Bookrunners and Underwriters DBS Bank Ltd. 12 Marina Boulevard Marina Bay Financial Centre Tower 3 Singapore 018982 Merrill Lynch (Singapore) Pte. Ltd. 50 Collyer Quay #14-01 OUE Bayfront Singapore 049321 Oversea-Chinese Banking Corporation Limited 65 Chulia Street #06-00 OCBC Centre Singapore 049513 x

- 22. Legal Advisers to our Company and the Over-allotment Option Provider as to Singapore law Allen & Gledhill LLP One Marina Boulevard #28-00 Singapore 018989 Legal Advisers to our Company as to Indonesia law Hadromi & Partners Law Firm Setiabudi Atrium, 2nd Floor, Suite 209A Jl. H.R. Rasuna Said Kav. 62 Jakarta 12920, Indonesia Legal Advisers to our Company as to Malaysia law Jeff Leong, Poon & Wong B-11-8, Level 11, Megan Avenue II Jalan Yap Kwan Seng 50450 Kuala Lumpur, Malaysia Legal Advisers to our Company as to Mexico law Basham, Ringe y Correa, S.C. Paseo de los Tamarindos 400-A 9° Piso Bosques de Las Lomas México D.F. Legal Advisers to the Joint Issue Managers, Bookrunners and Underwriters as to Singapore law WongPartnership LLP 12 Marina Boulevard Level 28 Marina Bay Financial Centre Tower 3 Singapore 018982 Legal Advisers to the Joint Issue Managers, Bookrunners and Underwriters as to United States federal securities law Sidley Austin LLP Level 31 Six Battery Road Singapore 049909 Independent Auditors Ernst & Young LLP Public Accountants and Chartered Accountants One Raffles Quay North Tower, Level 18 Singapore 048583 Partner-in-charge: Yee Woon Yim, Chartered Accountant Independent Financial Adviser KPMG Corporate Finance Pte Ltd 16 Raffles Quay #22-00 Hong Leong Building Singapore 048581 Independent Market Research Consultant Infield Systems Limited Suite 502 1 Alie Street London E1 8DE United Kingdom xi

- 23. Independent Valuer Clarkson Valuations Limited St. Magnus House 3 Lower Thames Street London EC3R 6HE United Kingdom Principal Bankers Bank of America NA, Singapore Branch 50 Collyer Quay #14-01 OUE Bayfront Singapore 049321 DBS Bank Ltd. 12 Marina Boulevard Marina Bay Financial Centre Tower 3 Singapore 018982 Oversea-Chinese Banking Corporation Limited 65 Chulia Street #06-00 OCBC Centre Singapore 049513 Receiving Bank DBS Bank Ltd. 12 Marina Boulevard Marina Bay Financial Centre Tower 3 Singapore 018982 xii

- 24. SUMMARY You should read the following summary together with the more detailed information regarding us and the Offering Shares being sold in this Offering, including our financial statements and related notes appearing elsewhere in this Prospectus. You should carefully consider, among other things, the matters discussed in “Risk Factors”. Overview We are the largest Asia-based international operator of offshore support vessels and one of the top five globally, based on Infield’s data on the number of vessels operated by us and the other major international providers of global support vessels, with a diversified fleet servicing offshore oil and gas exploration and production (“E&P”) activities. Our offshore support vessels perform anchor handling services, ocean towage and installation, ocean transportation, heavy-lift and offshore accommodation services. Our vessels also provide harbour towage and emergency response services. As of December 31, 2013 and as of the Latest Practicable Date, we operated a combined fleet of 112 and 110 vessels, respectively, including 45 and 47 vessels, respectively, owned by our joint ventures (of which, as of the Latest Practicable Date, one vessel is undergoing conversion into an accommodation vessel and two vessels are chartered by a joint venture as a charterer on long-term charters). This combined fleet comprises Anchor Handling Tug Supply Vessels (“AHTS”), Anchor Handling Tugs (“AHTs”), ocean-towing tugs, Platform Supply Vessels (“PSVs”), accommodation vessels, utility vessels and crane and deck barges. As of the Latest Practicable Date, we have on order and scheduled for delivery 15 vessels, comprising two deck cargo barges, two Azimuth Stern Drive (“ASD”) harbour tugs, three Dynamic Positioning (“DP”) 2 or DP2 accommodation vessels, three DP2 AHTS, two DP3 Semi-Submersible Accommodation Vessels (“SSAVs”), and three vessels which our joint ventures have on order. In addition, we have one vessel that is undergoing conversion into an accommodation vessel. Please see “Business – Vessels to be Delivered” for further details. Our fleet operates worldwide serving offshore oilfields in Asia, Africa and Latin America. We have provided vessels and services for projects involving many of the world’s major oil companies, as well as many large international offshore contractors, such as Saipem, Hyundai Heavy Industries, Technip and SapuraClough Offshore. We earn revenue primarily from time charters of our vessels. We also earn significant revenue from lump-sum project contracts for which our vessels are deployed. We manage and measure our business performance in four distinct operating segments which are the Offshore Supply Vessels (“OSV”) Segment, the Transportation and Installation (“T&I”) Segment, the Offshore Accommodation (“OA”) Segment and the Harbour Services and Emergency Response (“HSER”) Segment. See “Business” for further information on our business. 1

- 25. Our Competitive Strengths Largest Asia-based international operator with a diversified fleet of offshore support vessels We are the largest Asia-based international operator of offshore support vessels and one of the top five globally, based on Infield’s data on the number of vessels operated by us and the other major international providers of global support vessels. As of December 31, 2013 and as of the Latest Practicable Date, we operated a combined fleet of 112 and 110 vessels, respectively, including 45 and 47 vessels, respectively, owned by our joint ventures (of which, as of the Latest Practicable Date, one vessel is undergoing conversion into an accommodation vessel and two vessels are chartered by a joint venture as a charterer on long-term charters). This combined fleet comprises AHTS, AHTs, ocean-towing tugs, PSVs, accommodation vessels, utility vessels and crane and deck barges. As of the Latest Practicable Date, we have on order and scheduled for delivery 15 vessels, comprising two deck cargo barges, two ASD harbour tugs, three DP2 accommodation vessels, three DP2 AHTS, two DP3 SSAVs, and three vessels which our joint ventures have on order. In addition, we have one vessel that is undergoing conversion into an accommodation vessel. Please see “Business – Vessels to be Delivered” for further details. Our large and diverse fleet, coupled with our ability to provide value-added services (such as the added value in providing transportation services through our T&I Segment together with positioning and set-up services through our OSV Segment), enables us to deliver comprehensive solutions to our customers by leveraging on our multi-segment offshore capabilities to actively cross-sell our services and secure contracts that are otherwise difficult as a single service-provider, thereby setting us apart and positioning us favourably to compete for tenders. Our involvement across a wide scope of the offshore oilfield services through our different business segments enables us to better understand and respond to our customers’ needs and allows us to anticipate future offshore oilfield service needs. Our diversified fleet and service offerings enable us to achieve financial performance and resilience during industry downturns. We have been profitable every financial year since our business expansion in 2007. We constantly monitor demand for offshore services, charter rates, vessel types and fleet size through our involvement across the wide scope of offshore oilfield services through our different business segments. With this knowledge, we are able to optimise the portfolio mix of our fleet in order to better service our customers and respond in a timely manner to industry trends. For example, as at the Latest Practicable Date, we have ordered two DP3 SSAVs to cater to the increased demand for deepwater accommodation vessels. We believe this is a key competitive advantage that differentiates us from our competitors. 2

- 26. Global reach with a proven international operating track record We have a proven international operating track record over many years. As of the Latest Practicable Date, we have completed 53 floating system (including floating production storage and offloading vessels and structures (“FPSOs”)) transportation and installation contracts since 1991. Our operational track record allows us to meet the qualifying criteria in tender processes across various markets. Our diverse fleet of modern vessels allows greater cross-border operability and flexibility to operate in markets across various regions. Whilst our industry is international, most players often operate within the territorial waters of several different nations, each with its own unique set of local operational considerations and regulations. We believe we have an advantage over our competitors with our international track record and experience operating in all the different markets. We believe that the geographical diversification of our operations also reduces our dependence on and risk exposure to any single geographical market and/or customer. 3

- 27. Well-positioned to capture market opportunities across all our business segments We believe that each of our business segments is well-positioned to capture market opportunities. Offshore Supply Vessels We are one of the leading Asia-based operators of AHTS and PSVs with a fleet of 14 AHTS and 13 PSVs as at December 31, 2013 and 15 AHTS and 13 PSVs as at the Latest Practicable Date. According to Infield, we have the youngest deepwater AHTS and PSV fleet and the youngest midwater AHTS and PSV fleet globally, with an average age of 2.3 and 2.2 years, as at December 31, 2013, respectively. The age profile of our fleet is a key competitive advantage as modern vessels are often preferred due to better reliability and emphasis on higher environmental and safety standards. Our modern deepwater AHTS are well-placed to benefit from the growing demand for deepwater vessels arising from increased deepwater oil and gas E&P activity across the world. Furthermore, all of our AHTS and PSVs are equipped with Dynamic Positioning or DP technology which is increasingly a pre-requisite for most offshore projects. Transportation and Installation We are one of Asia’s leading operators providing deepwater towage services for various high-value offshore assets, such as rigs and FPSOs, and offshore construction, transportation and support services in the shallow-water segment. According to Infield, we have one of the largest deepwater AHT fleets in the world ranked by fleet size. We have built up a track record in completing many demanding and high-value ocean towage projects, having successfully completed 53 floating system (including FPSOs) transportation and installation contracts since 1991 as of the Latest Practicable Date. According to Infield, we have been involved in at least seven of the 35 floating unit installations that have taken place in Asia-Pacific between 2010 and 2013, including five of the 15 largest in terms of topside weight. In the first half of 2013, we were awarded the transportation and installation contract for Ichthys Central Processing Facility (“CP Facility”) as well as the Ichthys FPSO. Once the Ichthys CP Facility is completed, the structure is expected to be the world’s largest CP Facility installed to date. Offshore Accommodation As at the Latest Practicable Date, we have ordered two 750-person DP3 SSAVs. These vessels are scheduled to be delivered by the end of 2014. As at the Latest Practicable Date, we are in the final stages of procuring a charter contract for the commercial deployment of one of the vessels when it is delivered. The execution of the charter contract is pending the completion of due approval process of the counterparty. Notwithstanding, there is no assurance that the charter contract will ultimately be executed by the counterparty. Such vessels are expected to capture the rising demand for high-capacity and high-specification accommodation vessels specially catering to the deepwater segment. These vessels will have modern structural designs (including one of the largest offshore heli decks), technology (such as DP3) and equipment and will be certified as Comfort Class (DNV Notation (1A1) Ship shaped) by DNV by complying with strict noise and vibration control requirements. The specifications of these vessels include having a deck space of 2,000 square metres, a maximum deck load of 3,000 metric tonnes and 390 cabins of one, two or four persons. According to Infield, as at the close of 2013, there were only three operational SSAVs with berth capacity of more than 600-person and another three on order or under 4

- 28. construction (including our two 750-person DP3 SSAVs). According to Infield, upon the delivery of our two DP3 SSAVs, we will operate the youngest high-berth accommodation vessel fleet in the world. As at the Latest Practicable Date, we have also ordered three 238-person DP2 accommodation vessels, of which two are scheduled to be delivered by the end of 2014 and one is scheduled to be delivered by the first quarter of 2015. In addition, we have one vessel that is undergoing conversion into a 198-person accommodation vessel, which is expected to be delivered by the second quarter of 2014. When all of the accommodation vessels that are under construction or undergoing conversion are delivered by 2015, our accommodation capacity will increase from 879 persons as at the Latest Practicable Date to 3,291 persons (this includes one 191-person accommodation vessel that is committed for sale after the Latest Practicable Date). Harbour Services and Emergency Response Our Harbour Services business has been operating for over 10 years. We own, operate and manage a fleet of harbour tugs and heavy lift crane barges, which are actively engaged in supporting harbour towage operators and providing heavy lift services to shipyards engaged in the construction, and repair and conversion of ships and offshore drilling units, and other offshore structures and topside production and processing facilities. In November 2013, our subsidiary, POSH Semco Pte. Ltd. (“POSH Semco”), was granted a public licence by the Maritime and Port Authority of Singapore (“MPA”) for the provision of towage services to vessels within the limits of the port and the approaches to the port as described in “Government Regulations”. According to Infield, we are also one of the two main offshore support vessel operators globally to offer emergency response services which include salvage, wreck removal, rescue and oil-spill response services. Emergency, salvage and oil spill response services encompass emergency assistance to vessels that encounter grounding, collision, incidences of fire and oil spillage as a consequence of collisions and groundings. In particular, salvage refers to the process of recovering a vessel, its cargo, or other property after a shipwreck, grounding or other marine accidents or incidents, and encompasses refloating, towing and recovery of a sunken, grounded or incapacitated vessel. Established reputation and long-standing relationships with key oil and gas industry players As a result of our proven international operating track record, we have built a strong reputation and an extensive network of customers including global oil and gas majors and international oil and gas contractors. Leading global shipyards and offshore engineering companies, such as Saipem, Hyundai Heavy Industries, Technip and SapuraClough Offshore, also work with us on a regular basis. Our reputation and long-standing relationships with customers enable us to compete effectively and continue to grow our business. Strong parentage We believe that our Group benefits significantly from being a member of the KSL Group. Our parent, KSL, shares common heritage with two other holding companies, namely, Kerry Holdings Limited in Hong Kong and Kuok Brothers Sdn Bhd in Malaysia, in that they were all founded by the Kuok family, which together with their related companies, are commonly referred to as the Kuok Group. The Kuok Group is a well-regarded conglomerate with diversified investments in commodities, hospitality, logistics, real estate and shipping businesses, among others. The Kuok Group is the single largest shareholding group in listed companies such as Hong Kong-listed Kerry Properties Limited, Shangri-La Asia Ltd. and SCMP Group Ltd. (publisher of the South 5

- 29. China Morning Post), Singapore-listed Wilmar International Limited and Malaysia-listed PPB Group Berhad (“PPB”) and Malaysian Bulk Carriers Berhad (“MBC”). Our parentage makes us a preferred partner for leading local entities when we enter new markets or form strategic alliances. As the dedicated offshore support vessel business of the KSL Group, we have ready access to the affiliated shipyards of the KSL Group. We believe our strategic relationships with these shipyards will allow us to respond rapidly to changing market dynamics through quick turnaround times for newbuilds (although there is no publicly available information on the turnaround times for other shipyards) and manage our own maintenance and refurbishment costs as we enjoy operational advantages from our ready access to these shipyards such as the ability to gain a closer level of control and cooperation with the shipyards in terms of design and technical specifications, costing and procurement of equipment, and delivery timelines, as described below: • We are actively engaged in determining the design and technical specifications of the vessels. In this regard, the specifications of the vessels and the identification and costing of the various engines, parts and technical equipment (including replacement parts and equipment) are specified by us. We are actively involved in the procurement of such engines, parts and equipment (including identifying and selecting the suppliers and engaging in negotiations with such suppliers) prior to the shipyards placing the orders for and importing these engines, parts and equipment on our behalf for regulatory, operational and logistical convenience. In this way, we are able to gain a closer level of control over the costing of engines, parts and equipment (including replacement parts and equipment), which in turn translates into costs savings. • We station our technical superintendents in the shipyards as our vessels are being built, to monitor the construction and to ensure that the construction is correctly carried out in accordance with our approved designs and specifications and to further ensure timely delivery. • Another perspective of timely delivery relates to a scenario where we require vessels for a specific delivery in the future. This could be due to potential deployment or anticipation of a supply crunch for certain asset classes due to various reasons (for example, aging vessels scheduled for scrap etc.), and in this regard, not all shipyards may have available berths and capacity space to meet such future deliveries. • Not all shipyards are willing to build vessels to bespoke design specifications and have separate arrangements on the equipment package; instead, they prefer to build repeat designs, to benefit from their experience and economies of scale and gain discounts for their own benefit from equipment suppliers and manufacturers. Our transactions with the KSL Group are conducted on an arm’s length basis, as further detailed in the section on “Interested Person Transactions and Potential Conflicts of Interest”. Highly-experienced and committed management team with a proven track record We have a committed, experienced and highly-qualified management team led by our Chief Executive Officer and Executive Director, Mr. Seow Kang Hoe, Gerald who has more than 40 years of experience in the shipping industry (including 15 years of sea-going experience and more than 20 years of senior management experience), as further described in “Management – Directors”. Our Executive Officers come with varied and synergistic backgrounds – including Engineering, Marine and Finance – which enable them to lead and manage our Company. 6

- 30. Our management team includes 12 shore-based Master Mariners and 23 Chief Engineers with an aggregate sea-going experience of more than 600 years, as at the Latest Practicable Date. The depth and diversity of our management’s technical and operational expertise and experience enable us to identify, evaluate and capitalise on market opportunities and to better anticipate industry trends and invest in relevant assets to respond to our customers’ needs. In this regard, we have successfully expanded the scale of our fleet in terms of both capabilities and size (the vessels we operate grew from 98 vessels as at December 31, 2011 to 110 vessels as at the Latest Practicable Date, of which, as of the Latest Practicable Date, one vessel is undergoing conversion into an accommodation vessel). Our extensive experience and expertise in marine operations, marine engineering and fleet management allow us to proactively manage our fleet and achieve a high level of reliability, safety and efficiency in our operations. Recognising the technical capabilities required to operate and manage the two 750-person DP3 SSAVs which we have ordered as at the Latest Practicable Date and which are scheduled for delivery by the end of 2014, we have established an internationally-experienced management team with a proven track record. Heading this team is our Project Director, Operations, with more than 30 years of experience in North Sea and Latin America, including 17 years of handling day-to-day operations for four SSAVs. Strategy Broaden fleet diversification We look to continue to diversify our fleet and leverage on our multi-segment offshore capabilities to actively cross-sell our services and secure contracts that would otherwise be difficult as a single-service provider. We are enhancing our market-leading positions in each of our OSV, T&I and HSER Segments (as further described under “– Our Competitive Strengths – Well-positioned to capture market opportunities across all our business segments”), and also the capabilities of our OA Segment, by currently expanding our fleet through the acquisition of larger and more sophisticated vessels. As of the Latest Practicable Date, we have on order and scheduled for delivery 15 vessels, comprising two deck cargo barges, two ASD harbour tugs, three DP2 accommodation vessels, three DP2 AHTS, two DP3 SSAVs, and three vessels which our joint ventures have on order. In addition, we have one vessel that is undergoing conversion into an accommodation vessel. With respect to the OA Segment, recognising the technical capabilities required to operate and manage the DP3 SSAVs, we have established an internationally-experienced management team with a proven track record (as further described under “– Our Competitive Strengths – Highly-experienced and committed management team with a proven track record”). With respect to the HSER Segment, in November 2013, our subsidiary, POSH Semco, was granted a public licence by the MPA for the provision of towage services to vessels within the limits of the port and the approaches to the port as described in “Government Regulations”. Please see “Business – Vessels to be Delivered” for further details, including details on the contracted delivery date. Please also see “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Capital Expenditures and Divestments” for further details on our contractual commitments relating to vessels which our Company and our subsidiaries have on order and scheduled for delivery and how such committed future capital expenditures are expected to be funded. We adopt investment management processes in evaluating our fleet expansion plans. Factors which determine the level and timing of our fleet expansion include our assessment of the market demand and cost of investment for new vessels, our ability to secure attractive charter rates and 7