The Commercial Insurance and Reinsurance Markets

•

3 gefällt mir•3,127 views

For more information on the shifting landscape of the global commercial-insurance market, please visit: https://www.bcgperspectives.com/content/articles/insurance_perspectives_in_insurance/

Empfohlen

Empfohlen

Weitere ähnliche Inhalte

Mehr von Boston Consulting Group

Mehr von Boston Consulting Group (20)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

The Commercial Insurance and Reinsurance Markets

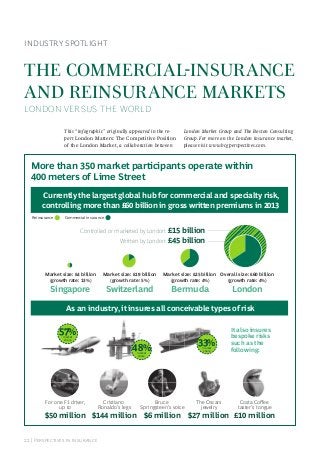

- 1. 22 | Perspectives in Insurance INDUSTRY SPOTLIGHT THE COMMERCIAL-INSURANCE AND REINSURANCE MARKETS LONDON VERSUS THE WORLD Currently the largest global hub for commercial and specialty risk, controlling more than £60 billion in gross written premiums in 2013 As an industry, it insures all conceivable types of risk Written by London: £45 billion Controlled or marketed by London: £15 billion Reinsurance Commercial insurance For one F1 driver, up to $50 million Cristiano Ronaldo’s legs $144 million Bruce Springsteen’s voice $6 million The Oscars jewelry $27 million Costa Coffee taster’s tongue £10 million 48%market share 57%market share 33%market share London Overall size: £60 billion (growth rate: 4%) Switzerland Market size: £19 billion (growth rate: 5%) Bermuda Market size: £25 billion (growth rate: 4%) Singapore Market size: £4 billion (growth rate: 13%) More than 350 market participants operate within 400 meters of Lime Street It also insures bespoke risks such as the following: This “infographic” originally appeared in the re- port London Matters: The Competitive Position of the London Market, a collaboration between London Market Group and The Boston Consulting Group. For more on the London insurance market, please visit www.bcgperspectives.com.

- 2. The Boston Consulting Group | 23 The market is a substantial contributor to the London economy 21% of the city’s GDP 8% of London’s GDP in 2013 … and supports the broader global economy by paying large claims every year professionals in London34,000 It employs 48,000 people… Another 14,000 work for London market companies in the UK, but outside of London Deepwater Horizon 2010 $600 million Japanese earthquake and tsunami 2011 $1.95 billion New Zealand earthquake 2011 $1.2 billion Australian floods 2011 $650 million More than £140 billion paid in claims in the past five years

- 3. UK and Irela nd change in London share +0.2 p.p. Ot her Americ as Africa Europe Australasia Asia In addition,London is not keeping pace with emerging-market growth:its share declined from 2013 through 2014 London is tracking market growth only in commercial insur- ance,while it is losing share in reinsurance Tracking share in casualty, property, motor, and marine Gaining share in aviation (+8%) and other (+1%) Losing share in energy (–3%) and reinsurance (–2%) 4% market growth 10% market growth 5% market growth 8% market growth 1% market growth 1% market growth 11% market growthchange in London share +5.8 p.p. change in London share +0.5 p.p. change in London share +0.5 p.p. change in London share +0.5 p.p. change in London share +1.3 p.p. change in London share +0.1 p.p. However, London’s unique position is under threat U.S .and Cana da 24 | Perspectives in Insurance—Industry Spotlight

- 4. The Boston Consulting Group | 25 This translates into six challenges to London’s position... 1 4 2 5 3 6 London needs to meet substantial unmet demand for new products and solutions, building on its reputation for innovation and flexibility in order to offset the commoditization of more traditional risks. London is losing share in reinsurance (from a 15% share in 2010 to a 13% share in 2013) as purchasing is increasingly centralized and emerging-market growth gains importance. The comparatively high regulatory burden on London market participants raises costs and could put London at a further price disadvantage should the burden become greater than the value of regulation to customers. London does not have a strong position in emerging markets, and its share of business in these markets declined by more than 20%— from 3.2% in 2010 to 2.5% in 2013. London’s expense ratios were 9 percentage points higher than those of its peers in 2013— driven by higher acquisition and transaction costs—putting it at a price disadvantage for more price-sensitive risks. The prolonged so-market cycle, propagated by the superabundance of capital and securitization of insurance risk, challenges London’s role as the supplier of additional capacity to meet local needs.

- 5. 26 | Perspectives in Insurance—Industry Spotlight 1 3 2 5 4 6 ... and six opportunities for London to enhance its position London can meet substantial unmet demand for new products and solutions, building on its reputation for innovation and flexibility in order to offset the commoditization of more traditional risks. London can reinforce its strength in expertise- based underwriting with improved analytical techniques to deliver value to customers, enable better selection of risk, and help retain more commoditized business. It can invest in marketing the strengths of the London market— particularly in emerging markets— to stimulate customer demand and encourage brokers and carriers to remove barriers to placement. It can reduce the cost of doing business by delivering on infrastructure activities, removing London-specific processes and realizing economies of shared service to increase competitiveness for commoditized risk. London can break down barriers to reinsurance and intermediation and develop the distribution network, creating an appropriate local presence that will allow it to compete more effectively in high-growth markets. London can embrace the rise of alternative capital in order to take advantage of deep capital markets, build capacity in capital-scarce lines, and protect against extended so-market cycles.