Chicago's office construction history...where are we now?

•

1 gefällt mir•321 views

The question has been coming up often these days about where office development stands in this cycle.

Empfohlen

Empfohlen

Weitere ähnliche Inhalte

Ähnlich wie Chicago's office construction history...where are we now?

Ähnlich wie Chicago's office construction history...where are we now? (10)

Mehr von Hailey Harrington

Mehr von Hailey Harrington (7)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

Chicago's office construction history...where are we now?

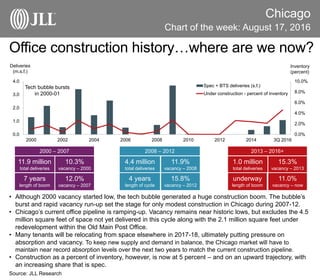

- 1. Chicago Chart of the week: August 17, 2016 Source: JLL Research Office construction history…where are we now? • Although 2000 vacancy started low, the tech bubble generated a huge construction boom. The bubble’s burst and rapid vacancy run-up set the stage for only modest construction in Chicago during 2007-12. • Chicago’s current office pipeline is ramping-up. Vacancy remains near historic lows, but excludes the 4.5 million square feet of space not yet delivered in this cycle along with the 2.1 million square feet under redevelopment within the Old Main Post Office. • Many tenants will be relocating from space elsewhere in 2017-18, ultimately putting pressure on absorption and vacancy. To keep new supply and demand in balance, the Chicago market will have to maintain near record absorption levels over the next two years to match the current construction pipeline. • Construction as a percent of inventory, however, is now at 5 percent – and on an upward trajectory, with an increasing share that is spec. 4.4 million total deliveries 4 years length of cycle 1.0 million total deliveries underway length of boom 11.9% vacancy – 2008 15.8% vacancy – 2012 15.3% vacancy – 2013 11.0% vacancy – now 2013 – 2016+2008 – 2012 11.9 million total deliveries 7 years length of boom 10.3% vacancy – 2000 12.0% vacancy – 2007 2000 – 2007 0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 0.0 1.0 2.0 3.0 4.0 2000 2002 2004 2006 2008 2010 2012 2014 3Q 2016 Spec + BTS deliveries (s.f.) Under construction - percent of inventory Deliveries (m.s.f.) Inventory (percent) Tech bubble bursts in 2000-01