Crypto Currency DAPMCOIN PROJECT WHITE PAPER: Killing two birds with one stone is the name of the game.

•

0 gefällt mir•255 views

Introduction of the DAPM COIN project: (DPCN) DPCN is a decentralized crypto currency or digital asset. DPCN has the same structures and uses as a digital currency or decentralized virtual asset. DPCN, currently found on the Ethereum platform will be traded around the world on the any Crypto Exchange that lists DAMPCOIN. DAP COIN was created by Danglo and Prieto Mining (Pty) LTD and was invented by the GLOBAL CEOAND EXECUTIVE DIRECTOR of Danglo and Prieto Mining, Ernesto Francisco Maposse.

Empfohlen

Empfohlen

Weitere ähnliche Inhalte

Was ist angesagt?

Was ist angesagt? (14)

Ähnlich wie Crypto Currency DAPMCOIN PROJECT WHITE PAPER: Killing two birds with one stone is the name of the game.

Ähnlich wie Crypto Currency DAPMCOIN PROJECT WHITE PAPER: Killing two birds with one stone is the name of the game. (20)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

Crypto Currency DAPMCOIN PROJECT WHITE PAPER: Killing two birds with one stone is the name of the game.

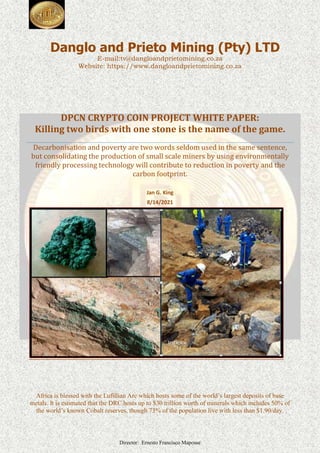

- 1. Director: Ernesto Francisco Maposse Danglo and Prieto Mining (Pty) LTD E-mail:tv@dangloandprietomining.co.za Website: https://www.dangloandprietomining.co.za DPCN CRYPTO COIN PROJECT WHITE PAPER: Killing two birds with one stone is the name of the game. Decarbonisation and poverty are two words seldom used in the same sentence, but consolidating the production of small scale miners by using environmentally friendly processing technology will contribute to reduction in poverty and the carbon footprint. Jan G. King 8/14/2021 Africa is blessed with the Lufillian Arc which hosts some of the world’s largest deposits of base metals. It is estimated that the DRC hosts up to $30 trillion worth of minerals which includes 50% of the world’s known Cobalt reserves, though 73% of the population live with less than $1.90/day.

- 2. Director: Ernesto Francisco Maposse 1 1. DISCLAIMER. This report may or may not contain certain “forward-looking statements”. All statements, other than statements of historical fact, which address activities, events or developments that DANGLO AND PRIETO MINING(Pty) Ltd believes, expects or anticipates will or may occur in the future, are forward looking statements. Forward-looking statements are often, but not always, identified by the use of words such as “seek”, “anticipate”, “believe”, “plan”, “estimate”, “targeting”, “expect”, and “intend” and statements that an event or result “may”, “will”, “can”, “should”, “could”, or “might” occur or be achieved and other similar expressions. These forward-looking statements, including those with respect to permitting and development timetables, mineral grades, metallurgical recoveries, potential production reflect the current internal projections, expectations or beliefs of DANGLO AND PRIETO MINING(PTY) LTD based on information currently available to DANGLO AND PRIETO MINING(PTY) LTD. Statements in this document that are forward-looking and involve numerous risks and uncertainties that could cause actual results to differ materially from expected results are based on the Company’s current beliefs and assumptions regarding a large number of factors affecting its business. Actual results may differ materially from expected results. There can be no assurance that (i) the Company has correctly measured or identified all of the factors affecting its business or the extent of their likely impact, (ii) the publicly available information with respect to these factors on which the Company’s analysis is based is complete or accurate, (iii) the Company’s analysis is correct or (iv) the Company’s strategy, which is based in part on this analysis, will be successful. DANGLO AND PRIETO MINING (PTY) LTD expressly disclaims any obligation to update or revise any such forward-looking statements. NO REPRESENTATION, WARRANTY OR LIABILITY Whilst it is provided in good faith, no representation or warranty is made by DANGLO AND PRIETO MINING (PTY) LTD or any of its advisers, agents or employees as to the accuracy, completeness, currency or reasonableness of the information in this report or provided in connection with it, including the accuracy or attainability of any Forward Looking Statements set out in this report. DANGLO AND PRIETO MINING (PTY) LTD does not accept any responsibility to inform you of any matter arising or coming to DANGLO AND PRIETO MINING (PTY) Ltd.’s notice after the date of this report which may affect any matter referred to in this report. Any liability of DANGLO AND PRIETO MINING(PTY) LTD, its advisers, agents and employees to you or to any other person or entity arising out of this announcement including pursuant to common law and the Companies Act no 71 of 2008 or any other applicable law is, to the maximum extent permitted by law, expressly disclaimed and excluded.

- 3. Director: Ernesto Francisco Maposse 2 Table of Contents 1. Disclaimer 1 2. Definitions, Abbreviations and Clarifications 3 3. Introduction to the project 4 4. Problems, Solutions and Product description 11 5. Introduction to Danglo and Prieto Mining (Pty) Ltd 21 6. Introduction to DAPM Coin (DPCN) 23 7. Introduction to TANZAMZAR INVESTMENTS (Pty) LTD 23 8. Summary of content 25 9. What is the normal process to start a mine? 26 10. The legal small scale mine 26 11. Containerised Modular Plant requirements 29 12. Heap Leach pads with centralised processing plants 32 13. The Kolwezi Dump and Kamfundwa mining project 35. 14. Summary of the project 41

- 4. Director: Ernesto Francisco Maposse 3 2. Definitions and abbreviations: 1. Africa: consist out of 51 countries as well as several Islands, however for the purpose of this document we want to narrow it down to the area defined as Sub-Sahara Africa, particularly the SADC countries. 2. Copper: Is a base metal in the greater collective called Battery metals. Although we will throughout this document use the word Copper, it will include metals like Cobalt, Zinc, Nickel, etc. 3. DRC: Democratic Republic of Congo. Throughout the document we will make use of DRC as an example because this is where his project will kick off, but countries like Zambia, Tanzania, Botswana, Namibia and South Africa, also offer investment opportunity in the battery metal space and it would mitigate risk. Once project 1 is operational, attention would move to alternatives to supplement and complement production. 4. ASM: Artisanal and Small scale Miners 5. Dump: Once processed the discarded material gets dumped on a designated place called a dump or Tailing Storage Facility (TSF). Some of these dumps are approaching 100 years of age and like with many things in life, improvement in techniques allow the extraction of metals and minerals from these dumps which were discarded, because it was uneconomical to extract or poor extraction methods at the time 6. DAPM: Danglo and Prieto Mining (Pty) Ltd 7. DPCN: Danglo and Prieto Mining coin 8. TANZAMINVEST: TANZAMZAR INVESTMENTS (Pty) LTD 9. EV: Electric Vehicle(s) 10. ESG: Environmental, Social and Governance matters. 11. HLP: Heap Leach Pad 12. CMP: Containerised Modular Plant 13. SX: Solvent Extraction 14. EW: Electro-Winning. 15. SX/EW: Solvent Extraction and Electro-Winning plant.

- 5. Director: Ernesto Francisco Maposse 4 3. Introduction to the Project: a. Decarbonisation to mitigate climate change: In 2021, the world’s attention has shifted toward the global drive to net zero, with the United Nations describing it as a “make or break year” for action on climate change. In 2020, net zero carbon commitments roughly doubled, with many countries embracing the opportunity to deliver “green stimulus” to support economic recovery post-COVID. And in November, world leaders will gather at COP26 to coordinate action to stop the rise in global temperatures. Decarbonisation has a big role to play. Reducing emissions and reaching “net zero” on a global level has been – and will continue to be – one of the world’s largest and most pressing challenges in the coming decades. With the effects of climate change – extreme weather events, polar ice cap melts, wildfires and droughts – becoming more frequent and more intense, it’s paramount that we take urgent action to tackle this problem and its associated impacts on environments, economies and societies around the globe. Decarbonisation is our overarching path to a net zero future and this “race to zero” comprises two complementary pathways. 1. The first pathway is about reducing the carbon footprint produced across every industry – from water and transport, to manufacturing and city precincts. 2. The second is by decarbonizing the gas and electricity systems that power them, which is commonly referred to as “the energy transition.” b. Access to Battery metals: At the heart of the decarbonising world, Copper will be ruling the roost. The supply deficit for Copper will be around 5 million tons by 2025-2030. BHP to double exploration spend as ups search for base metals – Miningmx This is approximately 15 years too late, considering it takes up to 10 years to develop a new mine. Glencore’s outgoing CEO, Ivan Glasenberg, said at a recent conference that the world would have to double copper production in order to meet demand over the next 30 years. “Today, the world consumes 30 million tons of copper per year and by the year 2050, following this trajectory, we’ve got to produce 60 million tons of copper per year,” he said. “If you look at the historical past 10 years, we’ve only added 500,000 tons per year … Do we have the projects? I don’t think so. I think it will be extremely difficult.” With the net zero drive, there is a total disconnect between what politicians and scientists want and what business could deliver.

- 6. Director: Ernesto Francisco Maposse 5 Green Copper: Research firm Fitch Solutions Country Risk and Industry predict that the market forecast for green copper will grow from 1.5-million tonnes in 2020 to five-million tonnes in 2030; and that green copper as a percentage of total copper demand will rise from about 5.6% this year to 15.7% in 2030. With a market shortfall of 5Mt per annum from 2025 to 2030 and total demand assumed to double from 31Mt on 2030 to 60Mt by 2050, the demand will outstrip supply for years to come. Now that we determined that Copper will be in short supply, we have to analyse the Climate friendly (battery) metals from an African perspective. Africa is richly endowed with most of the metals that will drive the promoted EV revolution. The most important factor which must be understood is that Africans have just as rich a tradition as the Western, Eastern and Middle Eastern cultures, although for some reason not always recognised or honoured by many people. Due to colonisation the African countries adopted a lot of the colonising countries’ traditions and don’t be surprised if you are served a proper English breakfast in most guesthouses even in the deep rural areas. But going out of the cities, where you will find almost everything you will find in the rest of the world like mobile phone and internet connectivity, you will find a population that still live a subsistence livelihood and communities honouring tribal systems. The questions we want to answer is how to find a way to allow these communities to continue living their chosen lifestyle AND benefit by the extraction of minerals in their chiefdom. I am not trying to change or criticize the way things are done in Africa or anywhere else in the world, either by the multinationals who spend large amounts of investors’ money building mines and extracting resources or to condemn them for their conduct; what I am advocating is exploring possibilities to do things differently. Playing from the same rule book, just reading it from a different perspective.

- 7. Director: Ernesto Francisco Maposse 6 By the end of this document I am sure that you will agree that it is possible to do things in your own way, share wealth, prosperity and provide a decent sustainable return to investors. Before we explore the alphabet soup of acronyms like EV’s, ESG, and SDG etc. we would like to make a short introduction of the market from an African perspective. The Electric Vehicle Market: Elon Musk will always be known as the person who broke the omnipotence of the oil multinationals by opening the hearts and minds of people to the possibility of driving around in a vehicle driven by an electric motor. This success story caused countries to jump on the bandwagon to impose specific targets, which forced other motor manufacturers to enter the space as well. Without going into detail, we can say that most countries are looking to have at least 30% of the total cars on their roads powered by an electric motor by 2030. In total the leading car manufacturers plan to produce more than 20 million electric vehicles per year from 2025. From 2030, 25 million electrically powered vehicles are expected, from 2040 even 60 million vehicles per year. Bloomberg expects that by 2040 at the latest every second new vehicle will be equipped with an electric drive. Considering that it takes approximately 36Kg of Copper to build one electric car and add to those busses, trucks and the required charging points; we are looking at lots of Copper. The renewable energy market: Although I am not convinced that all the renewable energy sources like solar, wind and hydro power has none or very limited long term negative effects, I agree that the world has to move away from oil and coal as primary sources of energy. We have the first hand evidence of the destruction caused by coal fired power generation plants after almost 100 years of existence. The first generations of windmills just highlighted the imminent problem of disposing of the blades which reached the end of their 25 year lifecycle; how to recycle these huge items. I am not a scientist, but I guess it is difficult to predict what the effects of light and heat reflection from solar farms built in arid areas or the results of changes in migration routes of birds and insects caused by windmills will have in the next

- 8. Director: Ernesto Francisco Maposse 7 50 years or so. Hope it’s not too late. There are other options like Nuclear and Molten Salt Thorium Reactors but it is not meant to be part of this discussion. To predict future demand for Copper is virtually impossible because of all the possible decarbonising theories. For instance, it takes 2. 5 – 6. 4 tonnes of Copper, depending on the design, per Megawatt to build one wind turbine distributed as follows; 1. Generator – 0,7 – 4,0 tonnes of copper 2. Cabling – 0,7 - 1,0 tonnes of copper 3. Transformers – 0,7 – 1,4 tonnes of copper If the decarbonising drive stays on course this alone could add another 1 million tons of Copper per year by 2030 to the demand. Energy Storage: The major problem with Wind and Solar energy generation is storage. Although there is a case for molten salt storage in the case of Solar it has a very limited time frame (three to four hours). The obvious solutions are batteries which can be built in a wide variety of shapes and sizes depending on the application. Vehicle batteries have very specific limitations when it comes to weight, size and require very quick charging capacity. In the quest to find suitable storage devices, the Lithium-ion battery emerged as the clear winner for now. One of the reasons for this is that the voltage within the lithium-ion battery is reached by exchanging lithium ions. Due to their high density, lithium- ion batteries deliver constant performance over the entire discharge period and have no so-called memory effect, i.e. successive loss of capacity over many years of use or frequent partial discharge. The name lithium-ion is only the generic term for a whole series of possible chemical structures, such as lithium cobalt (dioxide) battery, the lithium iron phosphate battery and less commonly the lithium titanite and the tin- sulphur lithium-ion battery. In the decentralized storage space we have the Vanadium redox battery as the clear leader. As miners we prefer to focus on the extraction and processing of battery metals rather than the technical application of one in respect of the other. It is not really as simple as that, we have to take cognicance of the fact that most batteries only require Cobalt in hydroxide form or sulphate and

- 9. Director: Ernesto Francisco Maposse 8 not metal. The Cobalt metal market only spans 20% of the total Cobalt market. Beneficiation to metal has its benefits, but it could be an overkill. Climate friendly (Battery) metals: The following metals are currently in use in different variants of batteries; 1. Copper 2. Cobalt 3. Nickel 4. Lithium 5. Vanadium 6. Zinc 7. Molybdenum 8. Manganese 9. And Graphite. The processing technology we propose for our processing can successfully extract the top 7 of the above mentioned metals. Our focus will be with Copper because in order to build a sustainable business it is best to have a product that will pay the bills through good and bad times. On-going research and development might also change the combination of metals used in battery technology which will impact the price. A good example is Cobalt which in 2018 ran away to almost $ 100,000/ton before retreating to $25,000/ton and recovered to its current level just over $50,000/ton. Expert opinion has it that it will take at least 30 years to find a substitute for Cobalt but it is not enough to specialise in Cobalt only. Cobalt is found as a by-product in most Copper and Nickel mines. So to summarise our immediate focus will be Copper, Cobalt and Nickel in that order. The processing technology will be discussed in more detail later in this document. Copper: People often lose track of the fact that Copper is still the most efficient metal to use to conduct electricity, so electric motors, generators, cable, conductors, you name it, requires copper and there is no tangible substitute.

- 10. Director: Ernesto Francisco Maposse 9 According to a report by Bernstein, the New York bank, the future demand for copper will be heavily influenced by the success to which world economies are able to decarbonise. This is owing to copper’s ‘climate-healing’ industrial applications. Depending on the decarbonisation targets favoured, the demand outlook for copper is going to be significant. c. Poverty: End users of metals, especially those originating from troubled jurisdictions like the DRC, are becoming more and more under scrutiny to ensure their ore is sourced responsibly. Investigations into child labour practises, poor and unsafe working conditions, illegal mining and profits not being spent on warfare are becoming daily threats to the sustainability of mining operations and are the biggest threat to the Artisanal and small scale operator (ASM). Poverty, inequality and living in and around the mining operations of Multi-National companies without any or very little improvement in daily living conditions forced the local populations in all countries in Africa to take their lives in their own hands and seize opportunities available to them. This in itself can lead to situations described above. Artisanal Coltan mining It is not uncommon to hear about police and even armies removing artisanal miners from mine properties where they try to make a living by recycling dump materials and tailings. Unfortunately, this is a complicated problem and cannot easily be solved. We have to look at it from all angles. The Multinationals have the responsibility to build Tailings Storage Facilities and dumps to comply with strict environmental and constructional requirements. These entities are designed to last hundreds of years and are usually an eyesore. Multi metallic orebodies contain metals and minerals which are sometimes or at times not commercially viable or the processes are inefficient which lead to valuable commodities being left behind. Uncontrolled, unmanaged, poorly executed and illegal extraction of commodities like in the case of some ASM’s can created dangerous conditions and situations which can cause the deaths of thousands if runaways happen, such as the disaster at the Vale dump in South America.

- 11. Director: Ernesto Francisco Maposse 10 It is estimated that over 200 000 people in the DRC and 40 million world-wide are making a living with their bare hands from artisanal and small scale mining. Indirectly 240 million people globally benefit from the proceeds of this type of mining. ASM accounts for 20% of global gold production, 80% of the world sapphire supply, 26% of tantalum production and 25% of tin production. All indispensable in our jewellery, laptops and smart phones. ASM is recognised by key global development organisations as having the potential to be a major development driver in some of the world’s poorest countries. Because ASM miners participate directly in the fruits of their labours most of the money remains locally in their immediate communities (in contrast to larger-scale mines where most of the money goes offshore). People gain the opportunity to develop skills they would otherwise be denied by lack of education and employment numbers are exponentially greater than in other vocations. Billions of dollars continue to flood the sector as government and industry try to solve what alternates between being seen as a major global problem or a major opportunity for poverty alleviation, depending on point of view. ASM is an incredibly complex topic. Nuanced and diverse. In recent years, with the rise of conscientious consumerism, the spotlight has been put on where the world’s largest brands source their raw materials. Think of jewellery, smart phones and laptops for example and where the gold, tin, tantalum and other minerals used to make them come from. As a result, many of the biggest companies in the world have scurried to validate their supply chains so they can’t be associated with human rights and labour market abuses often causing them to re- direct their raw materials sourcing back to the richer developing countries. Working with the miners rather than abandoning them because things get too hard. Haut Katanga Province in DRC with all the current mining licenses clearly depicted. Most of these licenses belong to citizens of DRC, most are under-developed, dormant or the owner wait for his lucky day when someone with a bag of money comes by.

- 12. Director: Ernesto Francisco Maposse 11 Re-concentrating global wealth among the top one percent of the world’s population and in so doing, causing more damage than good to the lives of some of the poorest people on the planet, is not really best practice. Picture and information credit to Hugh Brown best-selling author and documentary photographer. Visit www.garimpeirosproject.com for more information about his Garimpeiros Project. ASM is not all good, and it’s not all bad. The challenge for all of us is to be able to pull out the best bits of ASM, while sanitising the bad. 4. Problems, Solutions, and Product Description. a. Problems on Global scale: Securing enough of these metals has become an overriding concern for many Western countries now looking to invest in green technology industries as a driver of broader pandemic recovery. Access to raw materials has been identified as a major bottleneck to the green industrial strategy and raw materials projects, refining included, are viewed as strategic. Africa is richly endowed with most of the required commodities, but resources and infrastructure are prohibitive when it comes to sustainable supply of beneficiated product. b. Problems on Local scale: Africa is richly endowed with commodities and minerals but the populations remain poor. Although they have access to orebodies and/or own mines, they do not have access to capital to develop the mines to its full potential. The current available leach medium is Sulphuric acid which complicate the extraction of Copper for the average miner without the necessary Capital to build a processing plant.

- 13. Director: Ernesto Francisco Maposse 12 Sulphuric acid remains in the tailings and is a serious risk to ground water contamination. Although there are third party facilities available to process run of mine ore, the cost of transporting low grade ore is prohibitive and miners are often not rewarded for secondary metals present in the ore. c. Solutions: To find workable solutions you have to understand your place in the bigger picture: The players in our mining space: In order to understand the dynamics of our plan to deliver metal to the market we would like to introduce the different role players and how we see them being part of our value chain. I am going to start at the bottom working my way up. The local community: The communities mostly consist of between 1,000 and 2,000 family members lead by a chief (male of female) who received the leadership through hereditary succession. It is customary to introduce yourself to the chief by appointment and explain the reasons for your visit. When applying for a mining license a letter of permission from the chief must be included. The members of this community are keen to be employed by the mining company and are also hostile towards intruders. Intruders could be citizens of the same country being sourced in a different part of the country as well as expats imported for their expertise. This hostility will not necessarily lead to fights or war but it could be detrimental to your operation. The community live a subsistence lifestyle and will grab any opportunity to improve their livelihood. Most companies will as part of their social pact with the community provide assistance with expanding farming skills through training and funding. It is best to determine what the community wants rather than imposing predetermined programs used in other areas or countries. Communities receive benefits from operations like maintenance of roads which improve their access to markets, selling produce to the mine camp, access to electricity, water, etc. Most of the time these benefits are taken for granted so it is important to highlight it when communicating with them. In most cases mines assist with school transport, schools, clinics and other necessities as part of the social responsibility. As with everyone in the world, there are corrupt chiefs around, so paying of benefits should be tracked. Because of the anticipated scale of our operations, we will be working very close with the local community. Local Government: The nearest town also benefit by the existence of a mine. An influx of money without the accompanied goods and services leads to alcohol abuse followed by the resultant domestic and other violence. The mine owner cannot be held responsible to ensure this does not happen, social responsibility cost money but it can and will affect operations if left unchecked.

- 14. Director: Ernesto Francisco Maposse 13 Provincial Government: Mineral endowment has no boundaries. You could end up having operation in one or more provincial jurisdictions or even one mine straddling the border between two provinces or two countries. We found several chiefdoms overlapping country borders. Although the policies, licensing and other administration functions are usually controlled by government there are mining governance controlled by provincial office bearers. NOTE: Due to our chosen target market, we will be interacting mostly in the space described above, (bar the taxes and royalties, we will pay to treasury). We do believe that the difference we will be making especially within the tribal arena could create great opportunities in the alleviation of poverty. National Government: All the SADC countries where we chose to operate adopted the very transparent cadastre system where you can not only follow the progress of new applications, but also check the validity of license owners you might be negotiating with. Each Government has its own royalty, company tax, personal tax and VAT/GST regimes as well as investment protection and incentive schemes. It is important to understand these and make sure you abide by the rules and accrue the benefits. Government also have Environmental, Water use license and other applicable departments governing the mining industry in their respective countries. On the flip side, most Governments in Africa are under pressure to deliver bigger and better to their citizens. It is not uncommon to experience regime changes following national elections. Although sometimes against better judgement, governments impose rules they know are not achievable. A lot of countries push for beneficiation of product knowing full well that over 90% of their population does not have access to electricity. Beneficiation and electricity goes hand in hand. Renewable energy sources, especially mini hydro power should be our contribution to the electric grid. Globally the United Nations: The 17 Social Developmental Goals to transform our world were developed by the UN. Although most of these are goals are to be implemented by governments, listed below you will find how we could be of assistance by following our business model: GOAL DESCRIPTION PROPOSED ACTION GOAL 1: No Poverty By providing processing capacity to ASM’s, creating value by developing mines. GOAL 2: Zero Hunger Provide direct and indirect jobs to the ASM’s and the nearby community.

- 15. Director: Ernesto Francisco Maposse 14 GOAL 3: Good Health and Well-being Each mine require medical facilities which could be extended to the nearby community/ GOAL 4: Quality Education Job specific training can be provided despite a lack of quality education. GOAL 5: Gender Equality It is common for both males and females working in the artisanal mines, children should be cared for. GOAL 6: Clean Water and Sanitation Sourcing water for processing will automatically provide sources of potable water to communities GOAL 7: Affordable and Clean Energy Decentralised processing capacity will require additional sources of renewable energy GOAL 8: Decent Work and Economic Growth Uplifting the ASM, will naturally create opportunities for trading and farming into rural areas. GOAL 9: Industry, Innovation and Infrastructure By upgrading roads, environmentally friendly extraction technologies. GOAL 10: Reduced Inequality By providing equal opportunity, upliftment of community through training GOAL 11: Sustainable Cities and Communities N/A GOAL 12: Responsible Consumption and Production Adherence to best practices. GOAL 13: Climate Action By using environmentally friendly extraction technology and renewable energy. GOAL 14: Life Below Water Control of run-off water and no acid mine drainage GOAL 15: Life on Land Environmentally friendly policies GOAL 16: Peace and Justice Strong Institutions N/A GOAL 17: Partnerships to achieve the Goal Social responsibility programs. Part of the social responsibility plan would be to engage with NGO’s, the UN, and other partners who are specialists in these fields to enhance our performance through sponsoring and partnering in activities which could make a difference. Environmental, Social and Governance Matters (ESG) Mining companies, investors, traders, manufacturers as well as end users of products became very critical about Environmental, Social & Governance matters (ESG). Companies without adequate systems and controls in place and proven compliance during audits will become non investable. Shocking results were obtained in recent audits where after reporters and analysts accused miners of paying lip service to ESG matters. However the opposite should also be applicable: if you comply with ESG matters you should sell your product at a premium.

- 16. Director: Ernesto Francisco Maposse 15 Environmental: The environmental footprints left behind by mining companies are immense. Using personal experience of growing up in South Africa, I can relate to the results of Acid Mine Drainage (AMD) just outside of Randfontein in Gauteng Province. We used to swim and later enjoyed the social interaction at the place called Robertson Lake. Today barricaded off and totally inaccessible because of radio-active pollution caused by AMD on the Witwatersrand goldfields. The responsible companies are closed or left the country. We will introduce a patented environmentally friendly leach process to extract Copper, Cobalt and Nickel from our preferred sites. The preliminary tests indicate that we can achieve 92% recoveries with almost no dissolution of unwanted Fe, Al, Si, K, Ca and Mg at ambient temperature and pressure. Over and above the “green” processing we will also adhere strictly to the Environmental management plan as adopted in the Environmental Impact Assessment. Social: We have identified our social partners and are committed in walking the talk. Added to the above info about local communities should be knowledge and understanding about the lack of access to capital and expertise for these communities. If we look at the cadastre map of these countries you will realise that most of these licenses belong to small scale miners. They found green coloured rocks on a piece of land, got some “expert” advice from layman geologists and started dreaming big. Where desperation starts driving these communities you will find places where children join their parents in working these places. I am not apologising for this abuse I am highlight facts. I found places where women worked the dumps, while fathers we minding their children while acting as guards on these dumps. Due to the language barrier I could not discover exactly what was going on but I can tell you that there were no children working only playing. Not the ideal environment but I saw it myself. As a responsible miner we will ensure that our working places are properly fenced off preventing unauthorized access, employ as many people as possible and offer business opportunities like supply of food to camps, etc. to the local community. Governance: With the aftermath of State capture in South Africa it became clear that corruption can be found everywhere. Huge multi-nationals were found wanting with investigations into banks and legal institutions only starting now. With the perception that because everyone is doing it, it cannot and will not be condoned. We believe that in this day and age nothing can be hidden forever so rather keep on the right side from day one. Control systems, budgeting, accounting, procurement, auditing are some of the management controls to be implemented to close the doors for corrupt activity and fruitless and wasteful spending.

- 17. Director: Ernesto Francisco Maposse 16 Some of the items we would be reporting on are: King IV (2016) Compliance. IR:- Integrated Reporting: Financial Capital Manufactured Capital Intellectual Capital Human Capital Social and Relationship Capital Natural Capital Environmental and Social governance. Responsible Sourcing. IMPACT Management:- o What problem are you addressing? o What is your theory of change? o Who are you seeking to influence or benefit (target population)? o What benefits are you seeking to achieve? o When will you achieve them? (Time period) o How will you and others make this happen? (activities, strategies, resources) o Where and under what circumstances will you do your work? (context) o Why do you believe that your theory of change will prevail? (assumptions) o How strong is your leadership? o How does your business model look like? Is it scalable? o Impact. Our projects could become large enough that we could offer our investors a possible exit through public listing, therefore governance will be done at a standard that makes this possible from the start. d. Product description. The processing technologies: Metalleach Limited developed the following patented processes: 1. AmmLeach® 2. Hyper leach® The above processes can successfully extract metals such as: 1. Copper 2. Cobalt 3. Nickel 4. Zinc 5. Vanadium 6. Lithium 7. Molybdenum

- 18. Director: Ernesto Francisco Maposse 17 The processes further explained. AmmLeach® The AmmLeach® process is a proprietary ammonia based process for the selective extraction of base metals from amenable ore deposits and concentrates. The technology consists of the same three major stages as conventional sulfuric acid processes, i.e. leaching, solvent extraction (SX) and electro winning (EW). The leaching occurs in two steps, an ore specific pre-treatment, which converts the metals into a soluble form, and the main leaching step, which uses recycled raffinate (the portion of an original liquid that remains after other components have been dissolved by a solvent) from the SX stage. SX is used to separate and concentrate the metals, whilst also changing from ammoniacal media to acid sulphate media from which metals can be directly electro won using industry-standard unit operations. The AmmLeach® process has many advantages compared to conventional acid leaching. The primary difference from acid leaching is that the leaching is conducted in a moderately alkaline solution, which allows the use of AmmLeach® on high carbonate ores where acid consumption would be prohibitive. The major differential in reagent consumption for moderate to high (50 to >100kg acid per ton ore) acid consuming ores compared to using AmmLeach® (<5kg ammonia per ton ore), and the fact that, unlike acid leaching, undesirable metals and other impurities are either insoluble or significantly suppressed, leads to major capital and operating cost savings. One of the key advantages of the AmmLeach® process is that, unlike some new technologies, it requires no special purpose-built equipment. The AmmLeach® process can directly replace acid leaching in an existing operation. AmmLeach® technology is suitable for both low grade heap leaching and higher grade tank leaching; the choice is dictated by the grade and deposit economics. As mentioned, one of the major benefits is that the AmmLeach® process has an extremely high selectivity for the target metal over iron and manganese, which are insoluble under AmmLeach® conditions. Calcium solubility is also significantly suppressed by the presence of carbonate and

- 19. Director: Ernesto Francisco Maposse 18 extremely low sulphate levels in the leaching solutions. These features ensure that there are no potential problems due to jarosite or gypsum precipitation reducing permeability in the heap or scaling problems in the SX plant. Silica is also insoluble in the AmmLeach® process, removing problems associated with formation of unfilterable precipitates within an acid leach plant during pH adjustment and the need to handle high viscosity solutions. Ammonia, unlike acid, does not react with alumino silicates and Ferro silicates, whose products can cause drainage and permeability problems in heaps. Compared with previous ammoniacal processes, almost any ore mineralogy can be treated as the pre-treatment step is specific to each ore body and the whole AmmLeach® process is tailored to individual ore bodies. Thus far, it has been demonstrated on predominantly oxide ores but some sulfides have also been shown to leach after appropriate pre-treatment. This advance allows the treatment of mixed oxide-sulfide ores which are often present in the transition from weathered to un-weathered ore. As a project proceeds, the AmmLeach® process can be modified to cope with the changing mineralogy from oxide to sulfide without substantial capital expenditure. Polymetallic ores can also be processed by AmmLeach® with separation achieved using solvent extraction to separate metals and produce multiple revenue streams. The minimisation of ammonia transfer allows these metals to be recovered directly from their strip solutions by precipitation, crystallization or electro winning. Decommissioning of the heap is extremely simple as no neutralization is necessary and the potential for acid mine drainage is virtually eliminated. After final leaching the heap is simply washed to recover ammonia and then left to vegetate, with the residual ammonia acting as a fertiliser. The alkaline residue allows immediate application of cyanide leaching of gold and silver in ores where there is an economic precious metal content after removal of high cyanide consuming metals such as copper. Work is currently underway to incorporate precious metal recovery within

- 20. Director: Ernesto Francisco Maposse 19 the AmmLeach® process. Preliminary work on the leaching of cyanide consuming metals prior to precious metal leaching with cyanide looks highly promising. Applications: Copper Copper is the world’s most important base metal by value and its price is a bellwether of world industrial production. Global mined copper production is around 18Mtpa, approximately a quarter of which is produced from oxide ores using hydrometallurgy. The Company believes that its leaching technology has the potential to increase significantly the share of global copper produced using hydrometallurgical processes. Hydrometallurgically recovered copper is much more attractive to mine owners than the production of concentrates from sulphide ores as it results in the production of high value cathodes at the mine. When sold these realise almost 100% of the copper content, compared to concentrates where owners may receive up to 40% less. Zinc Global mined zinc production is around 12.7Mtpa. The vast majority (~95%) of world zinc metal production uses smelting to recover and refine zinc metal out of zinc-containing feed material such as zinc concentrates or zinc oxides. Development of a new hydrometallurgical process route for zinc oxides has the potential to simplify zinc refining. MetaLeach has developed a novel (patents applied for) process for the solvent extraction of zinc from ammoniacal solutions. Test work has shown that zinc can be efficiently extracted using commercially available reagents in a single stage and stripped with acid solutions, with better efficiency and greater selectivity than has previously been reported. The general flow sheet for the zinc process is straightforward and consists of leaching, purification and recovery stages. The nature of the leach stage depends upon a number of factors, notably the grade of ore and leaching kinetics. High grade, fast leaching ore would be readily accommodated by an agitated tank leach, whilst low grade, slow leaching ores would be better suited to heap leaching. Depending upon the product desired there may be no need for a solution purification stage, further simplifying the overall process flow sheet. A wide range of different oxide zinc mineralogies can be treated by AmmLeach®, including those with significant hemimorphite content which presently can only be treated using acid. The co-dissolution of silica and iron in the acid gives a very complex flow sheet. Although this AmmLeach® application is at an earlier stage of development than copper processing, the acid route requires ore containing >10% zinc to be economically viable, so for lower grade zinc oxide deposits of this type the benefits of the AmmLeach® process are absolute.

- 21. Director: Ernesto Francisco Maposse 20 Other target metals 1. Copper/Cobalt oxide deposits; 2. Nickel laterite (saprolite) deposits; 3. Gold/Copper oxides and Silver/Zinc oxides (alkali leaching); 4. Molybdenum oxides – testing underway Economics: The AmmLeach® process has the potential to significantly reduce costs at the mine site for a wide variety of copper projects. Absolute operating costs are dependent upon several variables, but a significant portion of the operating costs of any acid leaching operation is the cost of the sulphuric acid consumed. For the AmmLeach® process nearly all the ammonia reagent is recycled, with reagent consumption typically ~3kg/t of ore processed, an order of magnitude lower than even the most efficient acid leaching operations. The higher the acid consumption of the ore, the bigger the cost differential compared to the lower cost AmmLeach® process. This is largely determined by the order of magnitude difference in reagent consumption – for typically high acid consuming ores sulphuric acid consumption per ton of ore is over 40kg, compared to average ammonia consumption of only ~3kg/t. Processing plant capital costs for AmmLeach® are similar to acid heap leach operations of similar size as essentially the same equipment is used for both processes. Capital costs associated with the handling and supply of the reagent are dependent upon the mine location and the form of generation/supply. For many acid users, especially in remote locations, the safe supply of sulphuric acid is logistically difficult and prohibitively expensive. For example, the transport costs of sulphuric acid can be as much again as the delivered cost of acid to a port. In many instances, economics will dictate that the mine will have to build a sulphur burning sulphuric acid plant for the supply of acid, which is a significant capital cost. In addition, to regulate supply variations, acid storage tanks for around one month’s consumption, whether the mine makes its own or buys in acid, will be required; significantly adding to the capital cost. For AmmLeach® , the supply of ammonia can be either from ammonia gas where circumstances are favourable or, as is more likely for more remote locations, by using urea, which is available safely and readily in dry granular form as a fertiliser. In fact, this is the preferred way to transport ammonia fertilizer around the world. At the mine site a thermal hydrolysis plant that converts urea into ammonia would be built, the main operating cost for such a plant being electricity. Capital costs for a sulphur burning acid plant for an average acid consuming (~35kg/t of ore) copper oxide ore mine producing circa 50,000tpa copper are some four times those of a urea hydrolysis ammonia plant.

- 22. Director: Ernesto Francisco Maposse 21 Hyperleach® A proprietary ambient temperature and pressure process for the leaching and extraction of base metals from sulphide ores and concentrates. Because most base metal sulphide are processed to produce a concentrate at the mine site, with the associated selling costs and payment terms involved, there is considerable scope to do more on site processing to generate higher returns for mine owners. Indeed, in many cases miners may receive payment for as little as 60% of the in situ metal content of the concentrate. Possible applications: Heap Leaching Nickel sulphide ores Copper sulphide ores Native copper ores Mixed copper sulphide/oxide ores Copper-gold ores Uranium Molybdenum sulphide/oxide Tank Leaching Nickel sulphide concentrates Nickel mattes Copper flotation concentrates Arsenical copper ores Arsenical gold ores Gold bearing sulphide Concentrate cleaning PGM bearing sulphide/matte Molybdenum sulphide 5. Introduction to Danglo and Prieto Mining (DAPM) Website: TV - DPCN & DAPM - Danglo and Prieto Mining Conceptualised by Ernesto Maposse and Dorcas Motloung in 2010 and founded in 2016 Danglo and Prieto Mining (Pty) Ltd, company registration 2016/429005/07 and its sister South African company, with the same name in Mozambique with Registration no: 101249662 were duly registered. The purpose was to generate projects and business opportunities in providing jobs for our communities and people! DAPM created a detailed business plan to start a new venture since 2010, which was about exporting diamond and gold around the world. The realities of the sector forced DAPM to look at

- 23. Director: Ernesto Francisco Maposse 22 other options and from 2017 to 2018 DAPM entered into other new businesses and opportunities such as: a. Mining b. Agriculture c. Farming d. Fishing e. Charcoal And Wood Selling And Global Exportation f. Clay Bricks Manufacturing. g. Concrete Bricks Manufacturing. h. Mechanic and Panel Beating. i. Supermarket. j. Construction Materials Selling. All of these above mentioned business are successfully registered with their own management. DAPM Contact information: Despite the fact that DAPM’s attention got diverted away from their original plans, DAPM re- focused its vision to mining and battery metals in particular: OUR VISION: To become an investment company of choice, offering safe, profitable investment options through an Initial Coin Offering (ICO) with partners in the drive to Net Zero. As a dedicated mining investment company DAPM believe the road to decarbonisation and the race to net zero will be found through the sustainable and responsibly sourced metals in the battery metal space. NOTE: To achieve this objective DAPM aim to enter into an exclusive and binding Partnership with TANZAMZAR INVESTMENTS (Pty) LTD in projects that meet the criteria.

- 24. Director: Ernesto Francisco Maposse 23 6. Introduction of the DAPM COIN project: (DPCN) DPCN is a decentralized crypto currency or digital asset. DPCN has the same and uses structures as a digital currency or decentralized virtual asset. DPCN, currently found on the Etherium platform will on the . be traded around the world any Crypto Exchange that lists DAMPCOIN DAP COIN was and was invented by the GLOBAL CEO created by Danglo and Prieto Mining (Pty) LTD AND EXECUTIVE DIRECTOR of Danglo and Prieto Mining, Ernesto Francisco Maposse. He has extensive experience in crypto currencies on the African continent since 2010 and was part of several crypto currency coin projects. DAP COIN Total Market Cap: In order to create intrinsic value only 5,191,898 DPCN was created. Coins will be released to fund projects, earn returns and create value to its investors. Detailed plans will be provided later in this document. 7. Introduction to TANZAMZAR INVESTMENTS (Pty) LTD. TANZAMZAR INVESTMENTS (TANZAMINVEST) is a dynamic diversified Investment Company with an integrated approach with respect to the “Battery” metal value chain, seeking to disruptively extract worth from exploration to final product, not necessarily in that order. Our partnered environmentally friendly extraction technology can process the following metals successfully: Copper, Cobalt, Nickel, Vanadium, Zinc, and Lithium. The AmmLeach® process is a proprietary ammonia based process for the selective extraction of base metals from amenable ore deposits and concentrates. The technology consists of the same three major stages as conventional sulphuric acid processes, i.e. leaching, solvent extraction (SX) and electro winning (EW). The introduction of renewable energy sources on site, the benefit of an environmentally friendly extraction process which deliver optimum performance at ambient temperature and pressure assuring significant savings in both CAPEX and OPEX would enable TANZAMINVEST to successfully claim the mantle of producing “Green” metal. Add to this the potential to environmentally friendly leave zero footprint and operating emissions free, definitely attract a premium price for the will products we produce. TANZAMINVEST’s main objective is to find opportunities to optimise our relationship with Metalleach Limited by extracting Copper, Cobalt and other minerals and metals from run of mine ore or from dump material which could be tailings, slag or waste dumps. Extractive technologies improved by leaps and bounds and for many years Cobalt were left behind in tailings for economic reasons. A combination of the above factors contributed to the opportunity to harvest valuable commodities from these dumps by recycling them. Recycling dumps will also clean up the

- 25. Director: Ernesto Francisco Maposse 24 environmental damage caused by previous extraction technologies and avoid recurrence where this process will be introduced. Since our tailings will not contain any harmful substances it could also be used to backfill old workings. TANZAMINVEST’s carefully laid plans will allow ramping up to producing 120K tons of Copper cathodes plus other by-products in just five years after commencement of production. per annum Our Copper Mine Development, Funding and Purchase strategy will materialise as follows: Many Copper and other base metal mines in Africa are ripe for purchase or JV funding, mainly in DRC and Zambia. They are closed, on care and maintenance or operational to a certain extent, usually operated by locals, but may need some financial support, expertise or newer equipment, and definitely access to state of the art processing facilities. Mission: To produce Copper and other base metals without leaving an indelible scar in the area mined and without leaving harmful substances in the residues that could contaminate ground water, leading the way to NET ZERO mining. TANZAMINVEST subscribe to the UN’s sustainability development goals and believe that by taking processing capacity closer to the small scale miner significant impact can be made on the alleviation of poverty. Key Management Team Jan G King, CEO and founder. Jan is a seasoned deep level miner (24 years <3,500m in all aspects of the mining process), Process re-engineering and contractor in Africa with a demonstrated ability to introduce new technology in the mining process. His main specialities include building teams by using local talent instead of expensive ex-pat specialist skills. Website: TANZAMZAR INVESTMENTS – NET ZERO IS OUR AIM IN EVERYTHING WE DO (tanzaminvest.com) Personal page: Jan King | LinkedIn and TANZAMZAR INVESTMENTS: Company Page Admin | LinkedIn Victor Loreti, CFO. ACIS, CIBM, LCIBM, CIMA. National Diploma Cost and Management Accounting (WITS). Victor is a versatile and accomplished Financial Manager, Commercial Manager/Chief Financial Officer and deputy general manager with a demonstrated operational success and specialised expertise in International Mining and Exploration Companies. Personal Page: Victor Loreti | LinkedIn

- 26. Director: Ernesto Francisco Maposse 25 Technical Advisor: Alan M Clegg, Technical Advisor Pr Eng, MAIME, BSc Mining Engineering, MSAIMM. Alan is a Natural Resources & Energy Industry Professional with over 4 decades of experience gained from working natural resource development projects, industries and related supply industries in more than 40 African and in total 160 countries across all the continents. Personal Page: Our People « Metaleach Limited Website: Metaleach Limited Francois Lenge Geology qualification at University of Lubumbashi, Diploma in Mathematics & physics department, Metallurgy at MUTOSHI TECHNICAL INSTITUTE (GECAMINES, Kolwezi); Francois is an accomplished geologist specialising in the Katangan succession which hosts most of the Copper-Cobalt deposits in the DRC. Samples will be sourced, collect and report on the samples on which extensive mineralogical and chemical test work will be executed at the MetaLeach accredited Laboratories lead by Michael Plasskit, renowned Mineralogist, who undertakes and oversees Laboratory Amenability test works for Special Up-grading and Leaching Techniques on Cu, Co, and Ni Extraction Processes using all of MetaLeach Technologies for potential commercial applications and Prof Nicholas Welham an experienced metallurgical professional who has spent considerable time working on minerals related R&D projects for industry and is the principal inventor of the MetaLeach suite of patented process technologies. Additional skills and expertise will be hired on an “if-and-when required” basis with the focus on skills transfer. 8. Summary of content: To mitigate the effects of climate change and assist with economic recovery after COVID the world will embark on a decarbonisation drive to reach Net Zero. To achieve these targets, the demand for battery metals, in particular Copper will soar. The demand for Copper doubles every 20 to 30 years. Over the next 26 years from 2019 to 2044 the demand for Copper will exceed the total amount of Copper ever produced; that equates to 746Mt of Cu. Global Copper production from 1800BC to 2018AD were 730Mt. This estimate is based on historic facts and can be updated annually. Since the 2008 economic melt-down exploration activity was in a decline and very few new discoveries was made, which in turn will lead to a decline in the development of new mines. The decarbonisation drive prompted Ivan Glasenberg to state: “Today, the world consumes 30 million tons of copper per year and by the year 2050, following this trajectory, we’ve got to produce 60 million tons of copper per year,” he said. “If you look at the historical past 10

- 27. Director: Ernesto Francisco Maposse 26 years, we’ve only added 500,000 tons per year … Do we have the projects? I don’t think so. I think it will be extremely difficult.” With the non-existent mine development pipeline the obvious alternative becomes the artisanal and Small scale miner ASM. 9. What is the normal process to start a mine? The following is a short summary of the process to build an operational mine from start to finish. Find enough evidence to assume the possibility to find an economic viable orebody. License the area for prospecting. Do soil, sampling, trenching, geophysical survey. License the area for exploration. Continue soil sampling, trenching, and followed by drilling. Declare maiden resource compliant to the code Ni43-101/SAMREC/JORC depending on the preferred jurisdiction where funding will be raised. Do pre-feasibility Feasibility Bankable feasibility Raise Capital Build mine, plant, TSF and commission. This process can take 5 to 15 years and the project can change hands several times during this period. It is dependent on demand for the commodity, the price, the grade, the size of the resource, etc. It is important to understand this process when we discuss the plight of the ASM. 10. The legal small scale miner: By law this will consist of a private company registered in the jurisdiction it wants to operate in, which applied and was granted a legal license in terms of the mining laws of the country where they live. Without going into the minute details of the requirements, the owner must prove the existence of a possible mineralised orebody, obtain permission from the local chief and community and maintain annual fees. The mines are annually audited for compliance to the environmental management plan and are penalised for non-compliance. These miners often have to resort to manual extraction methods and target the high grade ores which then are transported over vast distances to the nearest processing facility. Proceeds are often just enough to pay the salaries of the workers and the process continues. Obstacles preventing these miners to succeed. Access to working capital can be considered the main problem, which leads to all the other problems like:

- 28. Director: Ernesto Francisco Maposse 27 o Lack of knowledge about the orebody, no drilling can take place. o No information for planning purposes. o No code compliant geological report that prove in-ground assets. o No finance to rent or buy capital equipment. o Low volumes, Poor efficiencies o High cost o Low income, because of inconsistent grades in ore sold. o High transport cost, reducing income. o Lack of business acumen. The reality is that there is no opportunity to create no momentum, positive cash flow, which eventually can lead to turning around fortunes. It is not uncommon that the owners of these mines are drowning in debt, mostly created by unpaid salaries, transport and other accounts not paid. What are the obstacles when dealing with small scale miners? The moment you engage with them you increase the value of their property and they don’t have money to pay you for your expertise or efforts. Without basic exploration work it is impossible to understand the potential of the tenement and can therefore not warrant expansion of production by introduction of equipment. Not every piece of green rock represent the next Katanga mine, but sometimes it is enough to make a decent living. What is the solution? The only way to protect any expenditure with resultant increase in value is to obtain shares in the license holding company. Proper due diligence is required before engagement and shareholders’ agreements must be thorough especially when it comes to conflict resolution and sale of shares. Initially it is also difficult to determine the value of a mine. The company could be heavily indebted increasing the risks. Slowly farming in interest, creating value and generating cash flow to enable original owners to contribute to the build-up of the company should be aimed for. By obtaining information like historical tons produced against, grades and embarking on a soil sampling and trenching exercise could help fast track a maiden resource declaration. It is imperative to create value as fast as possible to build or improve the balance sheet and a positive cash flow. Valuation: There are several methods to do a valuation of mining assets. The most effective will be to determine what price buyers are in general prepared to pay for a mine in different stadiums of development. If we evaluate M&A activity between 2008 and 2018 the following average determined the price at various levels of development were as follows:

- 29. Director: Ernesto Francisco Maposse 28 If we consider the current Copper price, which some predict could double in the next 5 to 10 years, compared to the average over the period 2008 to 2018; there is a 157% improvement. To move the 10 year period forward would distort everything again because of the massive price drops during the pandemic in 2020. We assumed that 1 tons of Copper is equal to 2205 pounds. This principle is simple to understand and easy to explain and although not everyone would agree to this, it is a common measure that could be used throughout. It is important to understand that in situ Copper will continuously increase in value until it finally becomes metal which can be sold at a LME based price. Selling metal should be the aim of every mine owner out there. Below the price graph for Copper from 1 January 2008 until 31 December 2018, with the red line indicating the approximate average price for that time. State of development Valuation at $/lb Valuation at $/ton Average Copper Price between 2008 & 2018 Current Copper price on 13 August 2021 % difference Adjusted price per lb adjusted price per ton Operating 0.14 $ 309 $ 6 000 $ 9 429 $ 157% 0.22 $ 485 $ Pre-production 0.10 $ 221 $ 6 000 $ 9 429 $ 157% 0.16 $ 347 $ Feasibility 0.09 $ 198 $ 6 000 $ 9 429 $ 157% 0.14 $ 312 $ Exploration 0.03 $ 66 $ 6 000 $ 9 429 $ 157% 0.05 $ 104 $

- 30. Director: Ernesto Francisco Maposse 29 Categories of Small scale miners. o Artisanal miners: These target high grade outcrops, dig mostly with pick and shovel, following the veins into the bowls of the earth. This I the most dangerous operations, very erratic and mostly only produce in the dry season. o Small scale operation: These operations are a bit better organised, larger scale but still targeting high grade veins. The mining gets more consistent results, but remain on the border line of profitability. Community members make huge sacrifices in the hope of a better life. o Medium scale operation: These are slightly mechanised, mining bigger volumes and require mechanical means to concentrate ore. At this stage the low grade which is uneconomical to transport are stockpiled. Due to a lack of exploration work, the mine runs out of minable ore or collapse due to unsafe mining methods. o Larger scale operations: At this level the exploration, planning and operation start getting organised and reach consistency. They still sell concentrate at third party processing facilities. Transport takes up the largest chunk of cost and the operation remains financially stressed. It is also a known fact that third party processors don’t always pay credits for other minerals contained in the ore. o Mining operation with processing: This is the stage where enough geological information is obtained to build a life of mine plan. The team put together a resource statement and if they can afford it, obtain the necessary validation from an expert to make it code compliant. This is also the time when a processing plant can be purchased to produce consistent high grade ore or even metal. Adding any form of processing capacity to the mix to any of these operations will in general double the revenue from selling metal rather than concentrate. However it is not as easy as it sounds. The first level of on-site processing is our in-house designed Containerised Modular Plant (CMP). 11. CMP Requirements: Containerised Modular Plants using the patented processing technology were designed around the following parameters for Copper only: 1. Throughput: 50,000 tons of ROM ore per month. 2. Grade: 1% 3. Recovery: 500 tons of cathodes per month. 4. Payback period: 5 years 5. Reserve required: 5,000,000 tons at 1% containing 50,000Mt of Cu. 6. Life of mine: 10 years 7. Budget price: $ 12 million.

- 31. Director: Ernesto Francisco Maposse 30 Note: This is a relatively small plant: plant feed of 100ton/hr. 20 hours per day; 25 days per month will process the required 50,000 tons per month throughput. A small quantity of civil works will be required in terms of concrete pads, etc. which will be left behind if and when the plant requires relocation. Otherwise the plant can be extended to double, treble or quadruple production if need be. Once a large enough resource is uncovered a larger capacity plant can be built and the CMP’s can be relocated. A Cobalt circuit can easily be added to the proposed plant, though I don’t have a budget figure for that yet. Adding value: In order to obtain a JORC or SAMREC aligned resource statement of the required 5 million tons requires the following work needs to be done: 1. Desktop study: Research all available information available. 2. Airborne geophysics of the larger area. 3. Soil sampling on the identified “hotspots” 4. Trenching 5. Drilling (only 100m holes, mostly RC, but a couple to obtain core for the geotechnical assessment of the rock to determine rock strength for pit design purposes. The next steps will be pit layout, TSF, Dumps, etc. Skills development: We have assembled a multi-functional, multi-disciplined team of highly qualified and experienced individuals who will oversee the start-up and growth of the project. This team will be responsible to put in place modules and assessments to train all the incumbents of positions required to run the operations nationally and internationally. This training will include locals to minimise the use of expats as well as succession planning. The planned rollout of plants over a five year period to reach the envisaged goal of 120 000 tons of Copper per year, will put huge demand on resources like management skills, project planning, engineering skills, general mining, etc. If we use DRC as an example the majority of licenses are spread over 600Km from East to West and around 350Km North to South. With only three main towns like Lubumbashi, Likasi and Kolwezi inside those perimeters it might become a nightmare to source and find the required skillsets.

- 32. Director: Ernesto Francisco Maposse 31 Herewith a reminder of area with the licenses: Most mine owners enjoy the comforts of the cities while relatively inexperienced workers keep the production going with limited resources and support. Expanding resources to enable deployment of CMP’s will place massive demands on the current human resources and should not be disposed of but rather trained to meet the new demands. Deployment of the project over several countries will definitely exacerbate the problem. Skills that will be in demand are: Head Office: Corporate governance Management Human Resources Finance Mineral Resource Management Project Management Procurement On Site: Management Mining Exploration Civil Engineering Mechanical Engineering Contract Management Geology The first operation in every country will also serve as a training unit where operators, artisans and other skills will be developed to be rolled out in other areas.

- 33. Director: Ernesto Francisco Maposse 32 Another method to overcome these challenges is to employ the assistance of Contractors to bridge these gaps. Transfer of skills will form part of the contract. Because the rollout can continue for several years, contracting companies can gain untold experience operating in different jurisdictions. Examples are as follows: Contract Mining Civil contractors for site preparation for plants, water reticulation, TSF construction, etc. Maintenance teams to take care of Shutdowns and general maintenance Project management teams Exploration drilling Rehabilitation of old dump sites, worked out pits and vegetation of new dumps and TSF. Energy All African countries are in short supply of Electricity. By moving further North, Africa is endowed with more water and during the rainy season there is a shortage of sunlight hours. We envisage the use of renewable energy sources to reduce the carbon footprint and hope to be some of the first producers of “Green” Copper. Small hydro power, solar and back-up by energy storage systems is in our opinion the way to go. Since we are in the mining game opportunities exist for relatively small operators to design, build, construct, operate and maintain power plants specifically aimed at our needs. This can be done on an IPP type arrangement over a 10 year period. We will not be averse to the idea to sell power to the local community if allowed. It must be stressed that in general over 90% of Africa’s population do not have access to electricity. NOTE: Although this seems to be a clear cut workable plan there are several reasons why it is very risky. Furthermore this will only work for the last two tiers of Artisanal and Small Scale Mining listed above. WHAT ABOUT THE REST? 12. Heap Leach Pads with Centralised Processing Plants To cater for the smaller scale miners, with the aim to expand their production to the capacity that warrant its own dedicated processing plant we conceptualised the Heap Leach Pad system. The system consists of a series of Heap Leach Pads on the mine(s), where after a couple of weeks of irrigation with a reagent and ammonia solution a Pregnant solution will be tapped off and transported to a centralised processing unit containing the Solvent Extraction (SX) and Electro- winning (EW) part of the plant to produce Copper cathode.

- 34. Director: Ernesto Francisco Maposse 33 The project can best be explained through the following couple of slides: The AmmLeach® process is preferred over the Sulphuric acid plant, because of the ease of use and inherent safety to the workers and environment. The push for “Green” Ammonia in conjunction with “green” hydrogen will further assist to improve the Net Zero credentials of this project. Herewith a visual representation of the Heap Leach Pad system on the mine, on the left and the possible layout to depict several HLP’s with a central Processing plant close to the nearest town. The next slide represents the mines we are currently in negotiations with and busy testing samples extracted from the mines. The interim results indicate that we would leach approximately 80% of

- 35. Director: Ernesto Francisco Maposse 34 the Copper and Cobalt in less than 4 weeks. The pads will be designed to contain 5Kt of ore at >3mm and <15mm to achieve optimum results. Of the five mines indicated only mine A has a non-compliant resource statement, which is still too small the warrant the construction of a CMP. Mine A has a stockpile of 23Kt at an average grade of 0.82% which could see through the first 5 months of Heap Leaching. The in-pit resource for oxide ore is 523Kt at 2.26% which could last 100 Months at 5Kt per month. Fast tracking exploration to double the current resource of 2.4Mt to exceed 5Mt will warrant the building of a CMP to process 50Kt per month.

- 36. Director: Ernesto Francisco Maposse 35 The advantages of using this system to upgrade resource firstly by declaration of a maiden code compliant resource, then doubling the resource can be summarised as below: NOTE: Although this could lead to the discovery of at least one, maybe more mines that could be turned into tier 2 or 3 mines, it remains too risky to embark on it as a standalone business. To negate the risk of the above we need at least two operations that could provide cash flow generating ability as well as long term value. We identified two projects that meet these criteria. Both are in the DRC. 13. The Kolwezi Dump and Kamfundwa mining project. The Kolwezi Dump Project. The Kolwezi Dump in the DRC is a shovel ready project because of work previously done a by third party for the current owner; which only requires some updating because it was originally done in 2016. The dump consists of a SAMREC indicated resource of 12Mt at 1.18% Cu and 0.27% Co containing 141,500 tons of Cu and 32,500 tons of Co. Before commencing with the project we will do the necessary test work to determine if the dump material is compatible with the AmmLeach® or HyperLeach® processes.

- 37. Director: Ernesto Francisco Maposse 36 The successful testing would result in significant savings and a complete different approach. Since we have done extensive testing over the whole Copperbelt area in both DRC and Zambia we prefer to use the following info to describe the way forward: A new BFS will be developed from information obtained after on-site inspections and development plans with funding requirements derived from that. The following are projections provided by the owner of the properties to invite investment. Summary of production ramp-up, cash flow and predicted profit at AISC of $2.50/lb.: The project NPV: $ 396 767 336 and IRR: 101% at a discount rate of 10% seem very high mainly because of the one off cost of capital and the short time period and could even increase exponentially if the last two or three phases can be funded from cash flow. The nature of the project leans itself to a quick return of investment to investors and shareholders and would not require continuous capital expenditure like a normal mine. TANZAMINVEST aims to spend its profits to develop the Kamfundwa project which is an early brownfields opportunity with huge potential once developed. The equipment could be relocated to other projects with ASM’s, since it will have Year 1 Year 2 Year 3 Year 4 Year 5 Total dump Total Plants 2 2 4 Total tons mined 1 080 000 2 520 000 2 880 000 2 880 000 2 640 000 12 000 000 Total Copper Production 10 800 25 200 28 800 28 800 26 400 120 000 Total Cobalt Production 1 350 3 150 3 600 3 600 3 300 15 000 Total revenue (millions) 120 $ 280 $ 320 $ 320 $ 294 $ 1 335 $ Total cost (millions) 59 $ 139 $ 158 $ 158 $ 145 $ 660 $ Profit (millions) 61 $ 142 $ 162 $ 162 $ 148 $ 675 $ Assumptions Planned Price/ton Planned price/lb Actual Price/ton on 29 June 2021 Actual Price per lb on 29 June 2022 Long- term projected price/ton Long-term projected price/lb Copper cathode Price 9 000 $ 4.09 $ 9 226 $ 4.19 $ 10 000 $ 4.54 $ Cobalt Price (propably hydroxide) 16 975 $ 7.72 $ 48 500 $ 22.05 $ 40 000 $ 18.18 $ AISC 5 500 $ 2.50 $ Planned Recoveries Copper 85% Cobalt 46% Returns NPV (millions) $ 396.77 Discount rate 10% IRR 101% Summary of activity during ramping up and depleting dump in 5 years Most open pit mines run at < $1.75/lb

- 38. Director: Ernesto Francisco Maposse 37 another 5 to 10 years life expectancy. Depending on the situation with access, we will also consider processing ASM ore together with dump material. Projected schedule for plant roll-out and cash burn. (US$ amounts are in millions in table below) The Kolwezi Dump total ramp up to full production will take 33 months and the dump will be depleted in five years. Investment required and potential sources of funds: Phase 1 A Seed Capital of $1 million which will cover the first three months required asap. Total amount drawn down over phase 1 A-D is $50 million, which will provide 25% of total shares in the project, with right of first refusal to invest in the Kamfundwa mining project. Phase 1B $15 million for the rest of phase 1, complete test work and designs Phase 1C $14 million for Site design and preparations Phase 1 D $20 million to build, ship, construct and commission plant Phase 2 $20 million to commission the second plant. Equity, debt or project, hedge finance Phase 3 $20 Million to commission the third plant Equity, debt or project, hedge finance Phase 4 $20 Million to commission the fourth plant Equity, debt or project, hedge finance Our aim is to minimize shareholder dilution and optimise returns in any way possible. Phase 2 to 4 will in all likelihood be financed through cash flow; however debt through project or hedge finance will also be consider protecting shareholder interest. In addition to above offer a free carry share of 5% in the Kamfundwa project. PHASE 2 PHASE 3 PHASE 4 -21 MONTHS DAY 1 + 6 MONTHS + 12 MONTHS + 18 MONTHS TOTAL INVESTMENT Receive initial samples, test, negotiate JV agreement, site inspections, validation of info, plan requirements, etc Design TSF (5 months) Final testing and design of plant Sign off, complete contracts, order pumps, pipes, shipping, etc. Site construction TSF preparation PLANT 1 build, ship, construct, commission FIRST COPPER/ COBALT JULY 2023 PLANT 2 build, ship, construct, commission + on-site preparations PLANT 3 build, ship, construct, commission + on-site preparations PLANT 4 build, ship, construct, commission + on-site preparations 1.00 $ 7.00 $ 7.00 $ 20.00 $ 20.00 $ 20.00 $ 20.00 $ 110.00 $ Now Jan-22 Jul-22 Jul-22 Jan-23 It is highly probable that the last three phases could be funded from cash flow - 12 MONTHS - 18 MONTHS 15.00 $ PHASE 1 Dates the above amounts are required